From the archive – “Gas is cheap” – or gas was cheap?

“Gas is cheap,” declared George Osborne is his budget announcement yesterday, in a nod to new planned government measures to encourage investment in new gas power stations.

The plans mean gas plants constructed over the next few years will be allowed to emit carbon dioxide freely for the next three decades. The UK is already heavily dependent on gas. In 2010, 43% of our entire energy consumption came from gas – compared to just 15% for coal.

The news that gas is cheap may come as a surprise to the analysts at UK electricity and gas markets regulator Ofgem – or indeed to any householders who received an energy bill in 2011. As Ofgem said in an analysis released in October of last year:

“Higher gas prices have been the main driver of increasing energy bills over the last eight years….”

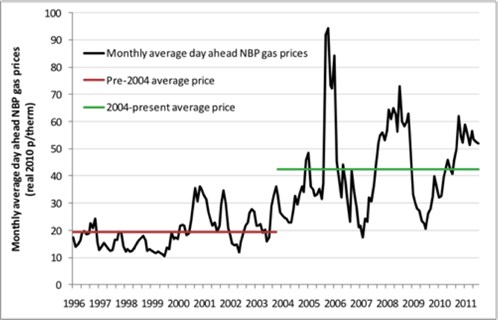

Would it be more accurate to say “gas was cheap”? The discovery of natural gas in the North Sea caused the oft-mentioned ‘dash for gas’ in the 1990s – a period during which gas prices fell markedly, as illustrated in this graph by Ofgem:

Image - Ofgem _gas _prices _graph (note)

{kind=link}

However, as the North Sea gas began to decline, the UK was increasingly forced to rely on imports from Norway and the Netherlands. As Ofgem puts it:

Britain enjoyed a period of falling gas prices until 2004/05. This is the year that Britain first imported more gas than it produced itself. Becoming more reliant on imported gas has meant that British gas prices have become increasingly influenced by global events…”

Future gas

But what about the future? It’s undoubtedly true that subsidies designed to increase uptake of green energy cost money. So isn’t gas the cheaper option in the longer term?

The UK currently gets about half of its gas from the North Sea, but if our gas demand stays about the same, by 2030 that figure will be less than a quarter. If we’re going to be burning cheap gas, it’s not going to come from the North Sea.

In the States, however, gas prices have fallen dramatically over the last five years due to the exploitation of indigenous shale gas. Some parts of the media have been arguing we can do the same, with claims that the UK could be “on the cusp of a new era of clean, cheap shale energy“.

Previous investigations have indicated that some of these claims might be somewhat overblown, although the debate is undoubtedly hampered by a lack of hard data. Last month, Ofgem released a report focused specifically on the impact of unconventional gas in Europe. The report was undertaken by the well-established energy consultancy Poyry and is probably the closest we’ve currently got to a relatively objective view on the subject. However there is one major difficulty – it was actually completed in June 2011, and the world of shale gas has moved on a bit since then.

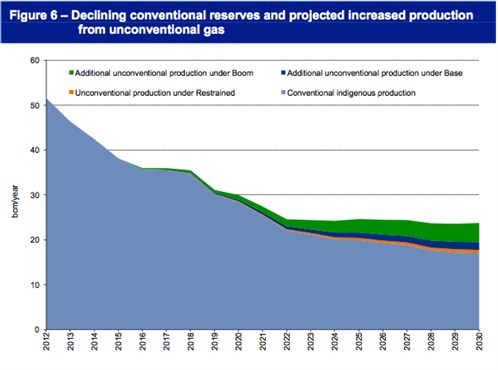

With respect to the amount of shale gas which we might be able to extract in the UK, Poyry relied on an estimate from the British Geological Society (BGS) of 144 billion cubic metres of shale gas – or about 1.5 years’ worth of gas demand at current levels. The consultancy modelled three different scenarios for what this might mean and displayed them alongside declining conventional production from the North Sea:

{kind=link}

Even under the ‘Boom’ scenario, the impact doesn’t look that significant.

Since the Ofgem/Poyry report was finalised in June 2011, however, the energy company Cuadrilla announced that it has discovered 200 trillion feet (or 5,600 billion cubic meters) in North West England – quite a lot more than the BGS estimated for the whole country.

What to make of this? As we have already noted, only 10-20% of Cuadrilla’s find may prove recoverable. BGS is reportedly skeptical about the accuracy of the estimate, and Cuadrilla clearly has an interest in talking up its find in order to increase the chances of getting a licence. The BGS is currently working on a new estimation for the amount of shale gas available in the UK, so it’s fair to say that the estimate in the Poyry/Ofgem report is out of date.

And of course, shale gas isn’t confined to the UK and the USA, but could be developed in many parts of the world. Under the report’s ‘boom’ scenario, for example, new sources of unconventional gas become available from continental Europe, USA production of shale gas increases and Australia exports liquified natural gas (LNG) to China and the Far East.

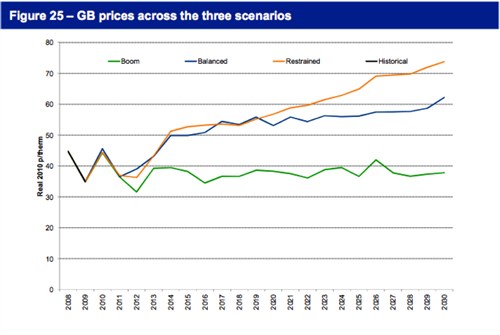

The report’s price projections for the different scenarios look like this:

{kind=link}

Again, this graph is somewhat inaccurate from the perspective of 2012 – a reflection of how tricky predicting future energy trends actually is. In 2011 gas prices did not fall as predicted in the graph above; they rose. According to the Department for Energy and Climate Change (DECC), gas prices were 63p/therm in 2011, not somewhere around 30-40p/therm as projected.

Do the prices in the graph above count as cheap? In the ‘restrained’ and ‘balanced’ scenarios, it doesn’t look like it. If we compare the projections for the ‘boom’ scenario to gas prices over the last twenty years, the answer is probably “cheap-ish” – cheaper than we experienced in the last ten years, but not as cheap as during the “dash for gas” in the 1990s:

Image - Wholesalegasprices (note)

{kind=link}

Source: DECC – Estimated impacts of energy and climate change policies on energy prices and bills (November 2011) p17

The rider on this is that Poyry also point out that, due to the probability of environmental concerns proving a “considerable hindrance to the development of unconventional gas resources in Europe”, the ‘boom’ scenario is a “low probability outcome”.

So where does that leave us? Frankly, it’s pretty hard to say. If the graph above tells us anything, it is that gas prices are a pretty unpredictable beast. Over the last year prices in the UK have been pushed up the Arab Spring (which pushed up the price of oil) and the Fukishima disaster (impacting on demand for gas). Even the most sophisticated economic models probably wouldn’t have captured that.

Shale gas has the potential to bring down prices the UK and elsewhere in Europe – but Poyry lists 14 separate issues that need to be addressed before commercial scale drilling could start. And even industry seems to agree that a significant amount of shale gas may not be a serious possibility for 15-20 years in Europe.

So – is gas cheap? It does seem to come down to the government spinning the roulette wheel of future prices. But having been following this for a while, we hope they’re feeling lucky.