Guest post: The era of ‘negative-subsidy’ offshore wind power has almost arrived

The offshore wind farms auctioned last September in the UK will most likely be the world’s first “negative subsidy” projects – wind farms that will pay money back to the government over their lifetime.

This is a key finding of our new paper for Nature Energy, which assesses the competitiveness of offshore wind in mature markets, without the support of subsidies.

The amount of renewable energy capacity is rapidly growing around the globe. At the same time, their specific investment costs are falling. Surprisingly, the prices received in recent auctions for offshore wind have already fallen below what analysts were predicting for 2050, some 30 years early. This fuels the controversial question of when renewable energy will reach the status of being “subsidy-free”.

In our new study, we find that offshore wind is already commercially competitive at good sites in mature markets, such as the UK. Thus, our analysis equips policymakers, academics and industry experts with evidence of an extraordinary story of success for a relatively young industry.

§ Offshore wind auctions

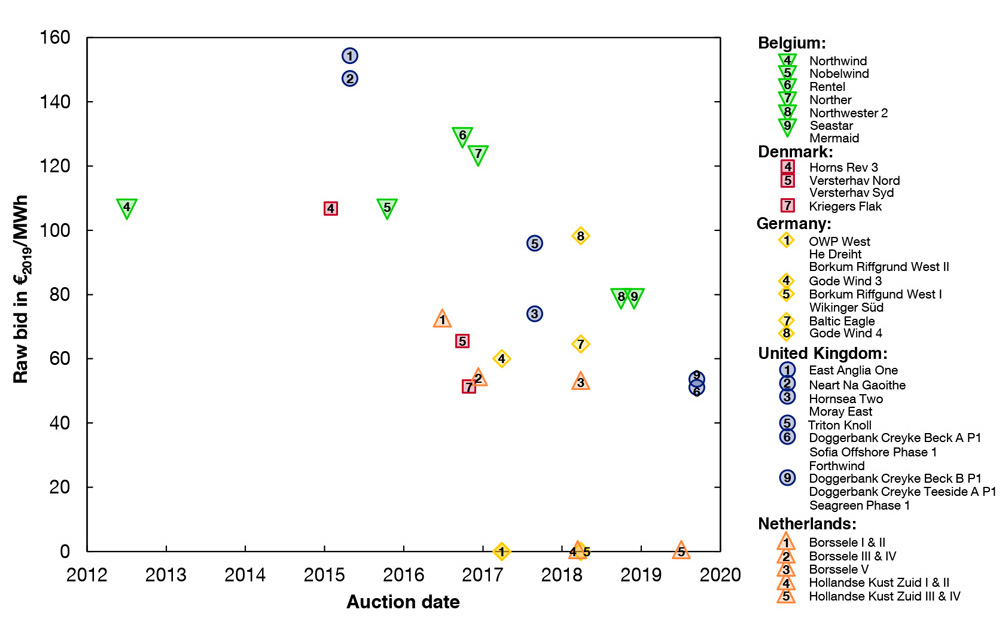

In our study, we focus on offshore wind projects that were auctioned from 2005 to 2019 in all countries that had held at least two auctions at the time of writing. This comes to 43 wind farms that won 17 auctions in five European countries, with a total capacity of 20 gigawatts (GW). This sample consists of different offshore wind technologies, including “monopile”, “gravity” and “jacket” foundations.

The figure below depicts the winning bids received in auctions for offshore capacity across five European countries. Each point shows the bid for a given wind farm against the date when the auction results were announced.

{kind=link}

However, a direct comparison of these auction results is a fruitless exercise. While a declining trend looks obvious, whether these bids are competitive depends on the details of the auction in question: How long are the subsidies paid? What revenues can be expected once auction payments end? Are grid connection costs covered? When will the project be built? Is it a one-sided or a two-sided contract for difference (CfD)?

(CfDs protect project developers from volatile wholesale prices and can include a subsidy. A one-sided contract offers a minimum price to the windfarm, whereas a two-sided CfD offers a guaranteed fixed price.)

§ Harmonising the data

{kind=link}

We analysed the winning bids using a monthly cash-flow analysis, accounting for the most significant factors influencing the costs and/or revenues of projects and, thus, influencing the bids received.

To do this, we defined the “harmonised expected revenue” metric, as the discounted average revenue per megawatt hour (MWh) of electricity generated over the lifetime of the project.

The metric incorporates all the money a wind farm can expect to earn, including revenues captured by a project when support has run out. This metric has two advantages.

First, it can be compared to wholesale prices (or LCOE of other technologies) as a non-subsidised benchmark. Second, harmonisation enables comparison for projects independent of country and auction set-up.

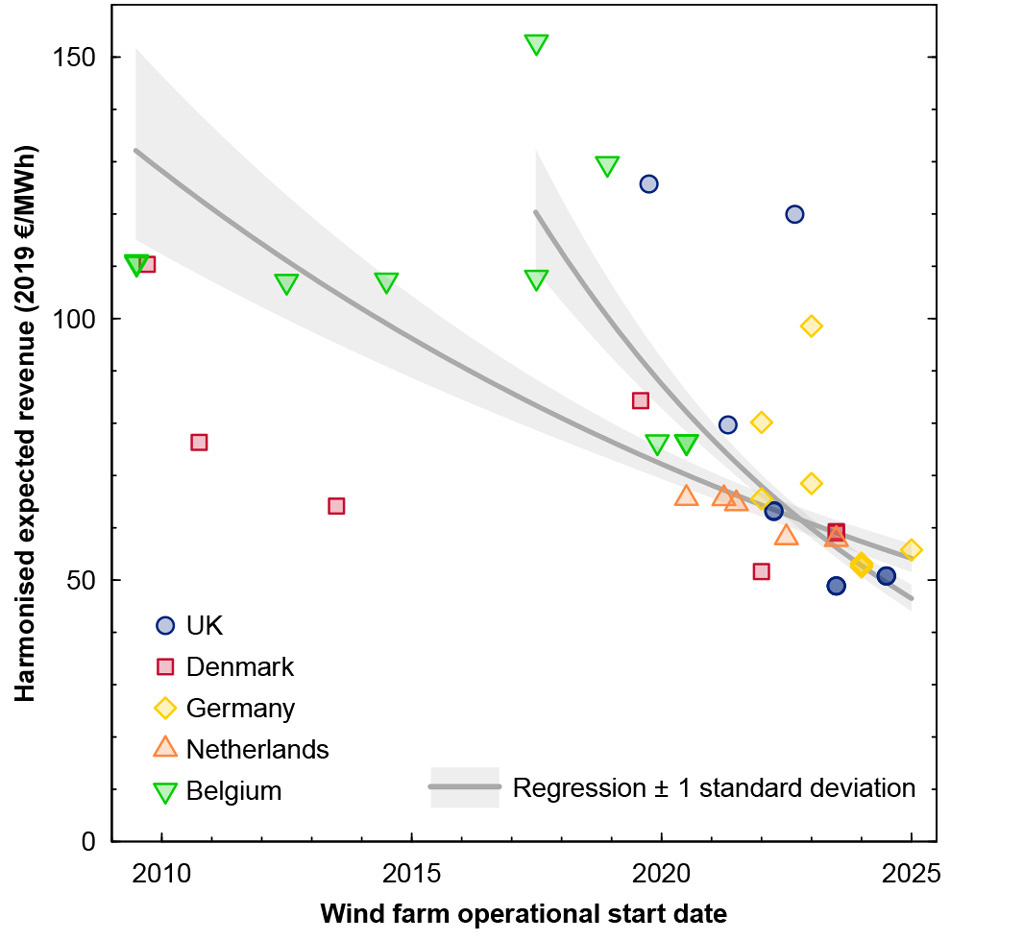

The chart below shows the harmonised expected revenues for each offshore wind farm auctioned in Europe – how much revenue they could expect to earn per unit of electricity produced over their lifetime Each symbol represents a wind farm, and the shaded lines show the trends over time, across all bids, and the most recent bids from 2015 onwards.

{kind=link}

What captures the eye is that wind farms due to be built after 2020 are converging towards a range of €50-70/MWh. This observation suggests that all countries are delivering consistently competitive bids, despite varying site conditions, auction criteria and levels of competition.

Another observation worth highlighting is that projects in three countries (Denmark, UK and Germany) have fallen below €50-55MWh, whereas the cheapest project in the UK is now below €50MWh. This suggests that the costs of offshore wind are at the lower end of estimated levelised cost of energy for fossil generators. However, such a comparison must be seen in the light of an ongoing debate around integration costs and market values.

Glossary: The levelised cost of energy (LCOE) is a measure of the unit energy cost over the full life of a project, including capital, operating and financing costs. In general terms, LCOE is calculated as the ratio between the lifetime costs of the energy project under consideration and lifetime energy production. LCOE is thus a cost per unit of energy.

§ A deeper look

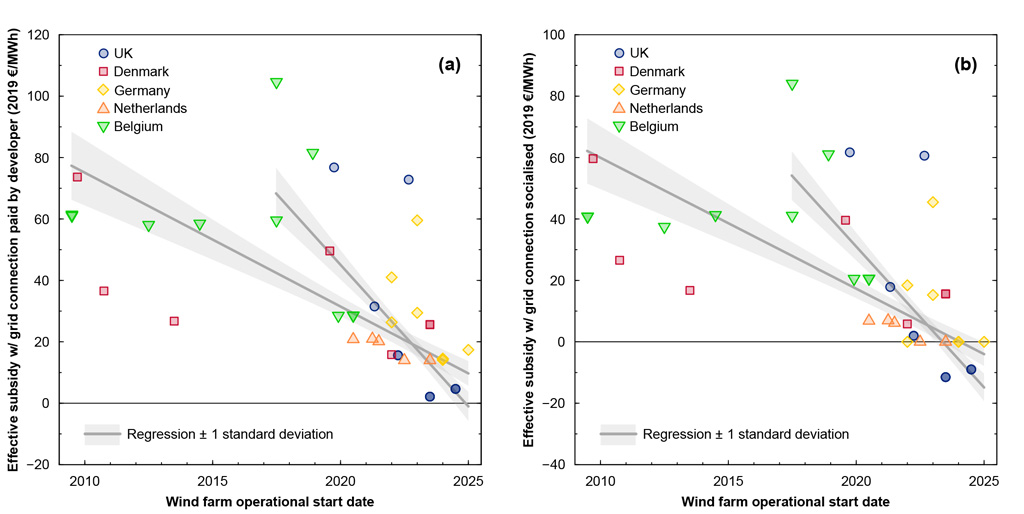

This level of subsidy depends on who should pay for the transmission cables that connect these remote wind farms to the grid.

One could argue that developers should pay as these links form an integral part of the wind farm, or that society should pay because transmission is part of the electricity network. Our study remains neutral and considers both cases in the figures below.

The figures show how much subsidy each wind farm could expect to receive over its lifetime and how this is decreasing with the newest farms to be auctioned.

The left panel shows the case where developers pay for transmission and the right panel case where society pays. In the right panel, the level of support going to wind farm developers is lower as this does not include the grid connection costs, which we estimate add around €13/MWh to the cost of offshore wind power.

{kind=link}

Note that if the expected harmonised bid is equal to the expected wholesale market price, the effective subsidy is zero and the project is subsidy-free.

What stands out in the figure above is that with socialised grid connection costs (panel b), offshore wind subsidies have reached –€12MWh for the latest UK auction. Furthermore, a large cluster of projects received an effective subsidy that lies in the range of –€10MWh and +€20MWh.

This important finding implies that several wind farms could expect to earn less money under the CfD support scheme than under wholesale market terms alone.

With the grid costs being paid for by the developer (panel a), the lowest effective subsidy is at €2MWh. However, we find that even slight growth in market prices (above 0.28% per year) will imply that this project requires no subsidy to operate.

§ Reaching a new era

Our analysis shows that the expected support for offshore wind projects has fallen by more than €5/MWh per year across all auctions. If the focus is narrowed down only to auctions from the past five years, the decrease is even more dramatic at more than €10/MWh per year.

This suggests that the era of subsidy-free wind farms will begin in 2023, based on recent auctions. But what is the impact of wholesale electricity prices?

The effective subsidy depends on how much the wind farm could earn on just the market alone. So, critically, it depends on the future development of wholesale electricity prices.

Expert analysis direct to your inbox.

Get a round-up of all the important articles and papers selected by Carbon Brief by email. Find out more about our newsletters here.

Get a round-up of all the important articles and papers selected by Carbon Brief by email. Find out more about our newsletters here.

Obtaining the correct medium- or long-term electricity price forecast is a challenging and controversial exercise for people in the industry. In our study, we addressed this issue by considering the sensitivity of our results to a wide range of wholesale power price trajectories.

The sensitivity test indicates that the UK’s latest offshore wind farms will receive a negative subsidy – and will be the first to pay money back to society – if wholesale prices grow at 0.3% per year above inflation. For context, prices have grown 0.8% faster than inflation over the past decade.

If grid construction costs are assumed to be socialised, UK offshore wind farms would be subsidy-free even if power prices fell by more than 1.5% each year in real terms.

§ Implications for the industry and beyond

Our study equips policymakers, academics and industry experts with the evidence that offshore wind will be a low-cost, low-carbon technology in the future. Hence, the initial spending made on support schemes has been successful in helping to create a new industry in this case.

We have highlighted that once bids are harmonised over the variations in auction design, the expected revenue streams of wind farms are similar across countries. This finding suggests that different auction designs were able to translate cost reductions into decreasing bids.

Our conclusions hold relevance for future wind auctions in Europe and beyond. In particular, policymakers in other continents could rely on the European evidence when designing the auction schemes for offshore wind.