Guest post: How China’s energy system can reach carbon neutrality before 2055

China’s thinking around the energy transition shifted drastically in 2020 after president Xi Jinping pledged to reach carbon neutrality before 2060.

Despite a series of major policy developments since then, however, it is still not clear what the new energy system will look like and which pathways are the most efficient for China to reach its carbon neutrality goal.

Our latest research models three scenarios for China’s energy transition: one in which China develops a net-zero emissions energy system before 2055; one in which it achieves this around 2055; and a baseline scenario that extrapolates current development trends.

We find that a combination of energy efficiency measures, electrification of end-use consumption and a low-carbon power supply based on various renewable energy sources – such as solar and wind – can greatly help the country to achieve its decarbonisation goals by 2055.

In the most ambitious scenario, China’s power sector will be fossil fuel-free by 2055, while some industries will continue to use a small amount of coal and gas. However, this will be balanced by negative emissions from biomass power plants fitted with carbon capture and storage (BECCS).

- How the dual carbon targets changed the game

- Three scenarios for China’s energy transformation

- Three phases in China’s energy transformation

- Coal power plants become flexibility providers

- Managing a grid dominated by variable wind and solar

- Visions for the future

§ How the dual carbon targets changed the game

When Xi began his speech at the UN General Assembly in September 2020, few had expected him to deliver such a ground-breaking announcement.

In his words: “We aim to have CO2 [carbon dioxide] emissions peak before 2030 and achieve carbon neutrality before 2060.”

This policy is now more commonly known as the “dual carbon” goals.

That one sentence changed the whole understanding of the energy transformation in China.

Until then, China’s target was to “promote a revolution in energy production and consumption, and build an energy sector that is clean, low-carbon, safe and efficient”, as Xi had said at the 19th National Congress of the Communist Party in China (CPC) in October 2017.

Xi’s 2020 speech shifted China’s priorities from reaching “low-carbon” to reaching “carbon neutrality”, from an energy sector that includes at least some fossil fuel consumption, to an energy sector which leaves little room for coal, oil and gas once carbon neutrality is reached.

The difference required a genuine change of mindset throughout China’s political system and stakeholders within the energy system, such as major power producers.

China started this immediately after the announcement: the State Council, China’s top administrative body, introduced the 1+N policy strategy, which is comprised of an overarching guideline for reaching the “dual carbon” goals (the “1”) and a number of more concrete guidelines and regulations to implement the strategy (the “N”).

So far, the policies have mainly focused on reaching the carbon peak before 2030 – but the long-term goal of carbon neutrality by 2060 is ever-present.

The National Energy Administration (NEA) has launched a blueprint for a new type of power system. At a broader level, several government departments have outlined efforts to transform the entire energy system, as opposed to just the power system, in the effort to reach carbon neutrality.

Hence, the foundation for China’s energy transformation is much more solid and precise today than it was before Xi’s announcement. The question now is: what will the new type of energy system look like and how will China reach it?

§ Three scenarios for China’s energy transformation

To answer these questions, our programme modelled three scenarios for China’s energy transformation: one in which China develops a net-zero emissions energy system before 2055; one in which it achieves this around 2055; and a baseline scenario that extrapolates current development trends.

The analysis is based on a detailed bottom-up modelling approach, while, at the same time, using visions for a “Beautiful China” – an official initiative for “the nation’s green and high-quality growth” – as guidelines for the transformation.

In our modelling, the overarching strategy for the energy transformation consists of three intertwined actions:

- Increase energy efficiency throughout the supply chain.

- Electrify the end-use sectors as much as possible.

- Transform the power sector into a “green”, fossil-free sector with solar and wind power as the backbone of the system.

(The Intergovernmental Panel on Climate Change’s latest assessment report showed that these are key elements of all global pathways that limit warming to 1.5C or 2C.)

A consequence of following this strategy would be that the Chinese energy system would be able to provide energy for sustainable economic growth in China with net-zero carbon emissions, improved air quality and a high level of energy security.

In the most ambitious scenario, the Chinese power system would be carbon-neutral from 2045 – and the whole energy system before 2055.

Compared to today, total primary energy consumption would be lower in 2060 despite economic growth. Moreover, coal, oil and gas would be practically phased out of the system – and dependence on imported fossil fuels would be eliminated.

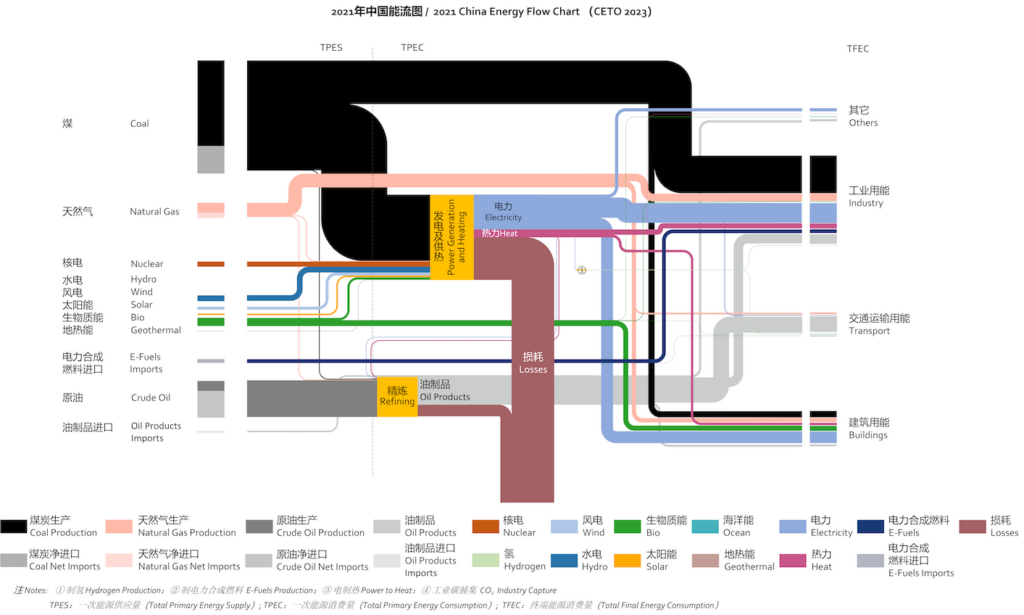

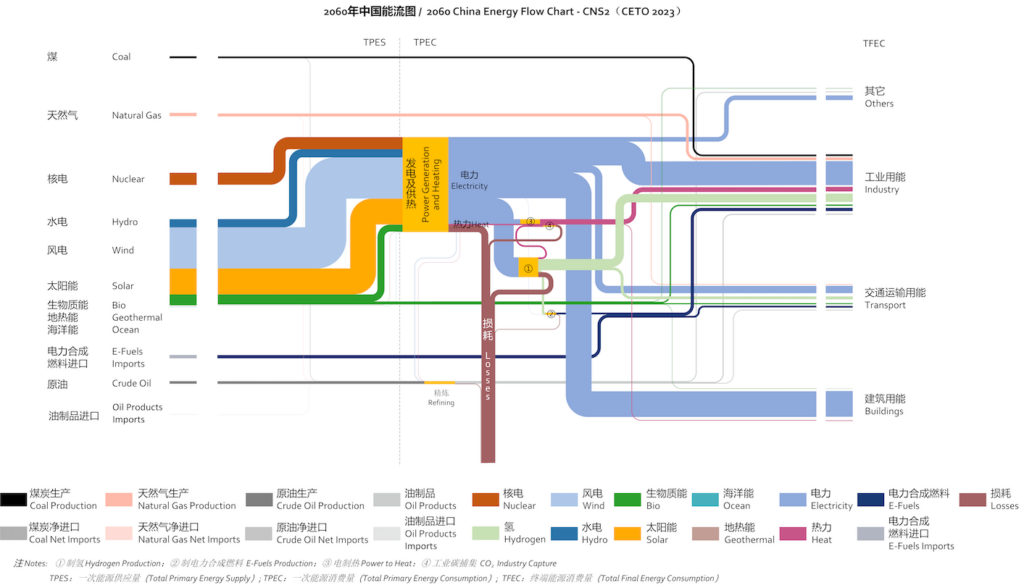

The figure below shows the energy flowing through China’s economy in 2021 (upper panel) compared with the energy flow in 2060 under this most ambitious scenario (lower panel).

On the left, each panel shows sources of primary energy flowing into the economy such as coal (black), gas (pink), oil (shades of grey) and non-fossil fuels such as nuclear (brown), hydro (dark blue), wind (light blue) and solar (yellow).

The centre of each panel illustrates the transformation of primary energy into more useful forms, such as electricity or refined oil products. Much of the primary energy contained in fossil fuels is wasted at this stage (“losses”) in the form of waste heat.

On the right, the users of final energy are broken down by sector.

Most notably, fossil fuels – particularly coal – are the largest sources of energy in 2021, whereas in the ambitious 2060 scenario, below, low-carbon sources dominate.

{kind=link}

{kind=link}

§ Three phases in China’s energy transformation

Our study suggests the transformation pathway will have three main phases. The first phase is the peaking phase until 2030.

During this period, the deployment of wind and solar power would continue to increase, while electrification of the industry and transport sectors would gain momentum.

However, coal and oil would remain the dominant energy sources in terms of total primary energy consumption.

Next is the “energy revolution” phase, from 2030 to 2050. During this phase, solar and wind power would become the main energy sources for electricity supply, and the electrification of the end-use sectors would be substantial.

The shift away from fossil fuels minimises the loss of waste heat in electricity generation and refining. Meanwhile, “green hydrogen” made from renewable power would become increasingly important in the industrial sectors.

The third phase is the consolidation phase, from 2050 to 2060. Decarbonisation occurs in sub-sectors that are challenging to electrify, such as the steel and chemicals industries, the old solar and wind power plants are replaced by new solar and wind power, and remaining fossil fuels in the energy mix are nearly phased out.

§ Coal power plants become flexibility providers

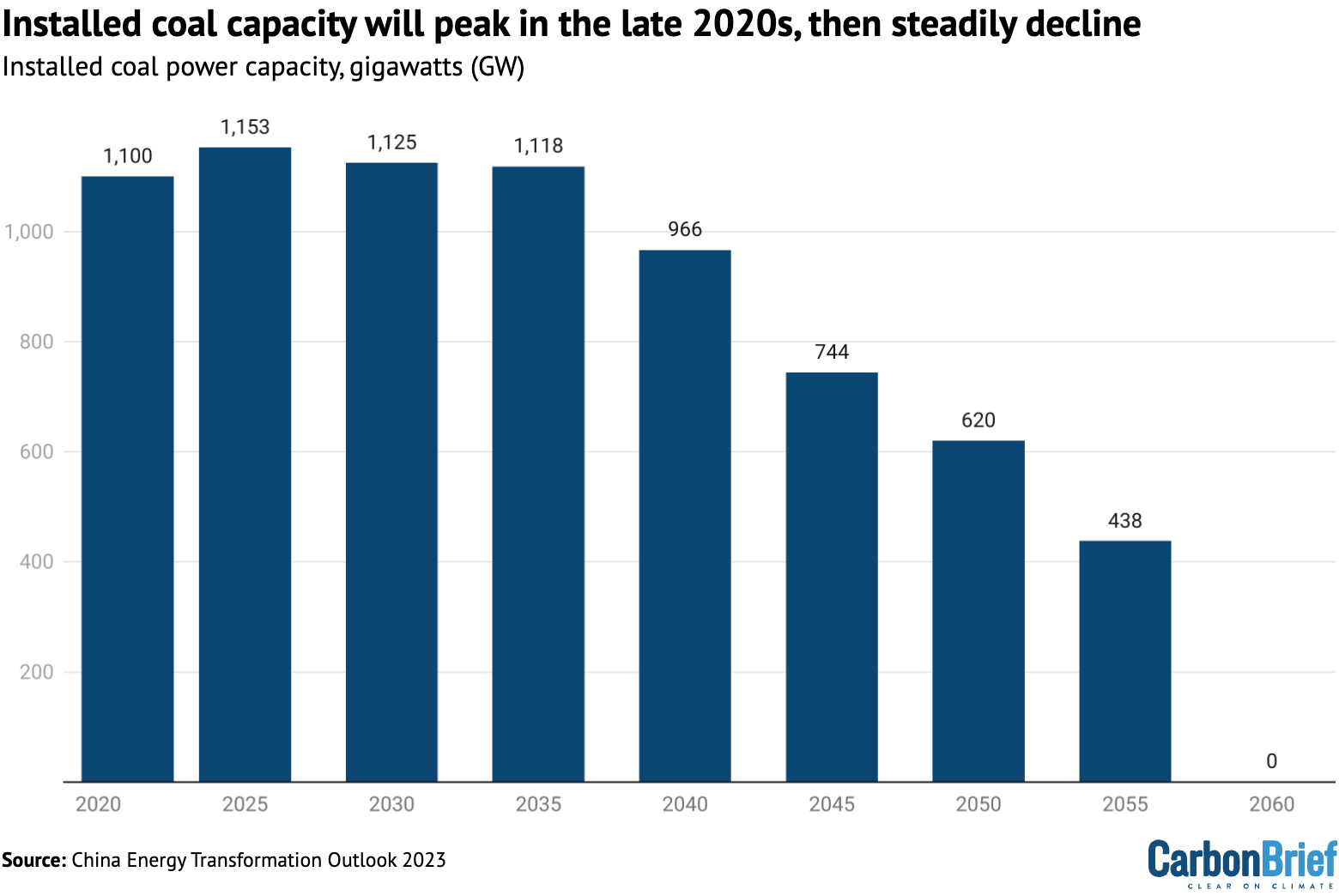

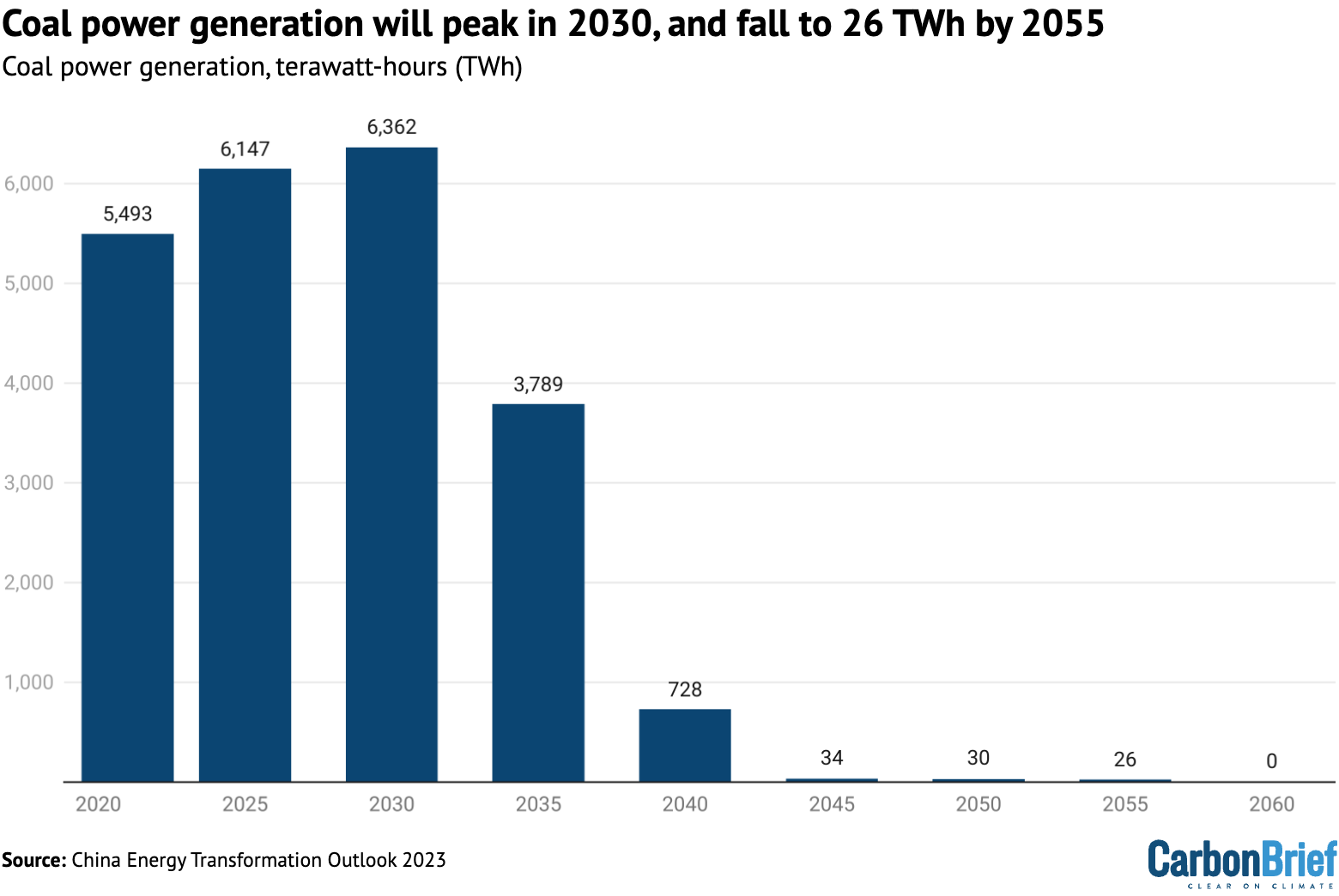

Although the Chinese government plans to “phase down” coal from 2025, based on the current policy guidelines and market situation, we estimate that coal power capacity would not be rapidly removed in any of our three scenarios.

Instead, coal power plants would gradually become providers of energy security and capacity to meet peaks in electricity demand, and not generate large amounts of electricity.

By the time they reach the end of their expected lifetime of around 30 years, the plants would be shut down and not replaced with new coal capacity. In our most ambitious scenario, the last coal power plants are closed in 2055, as shown in the figure below.

The upper panel in the figure shows the installed capacity of coal power plants and the lower panel their electricity production from 2021 to 2060.

{kind=link}

{kind=link}

Meanwhile, gas does not play a significant role in the power sector in our scenarios, as solar and wind can provide cheaper electricity while existing coal power plants – together with scaled-up expansion of energy storage and demand-side response facilities – can provide sufficient flexibility and peak-load capacity.

§ Managing a grid dominated by variable wind and solar

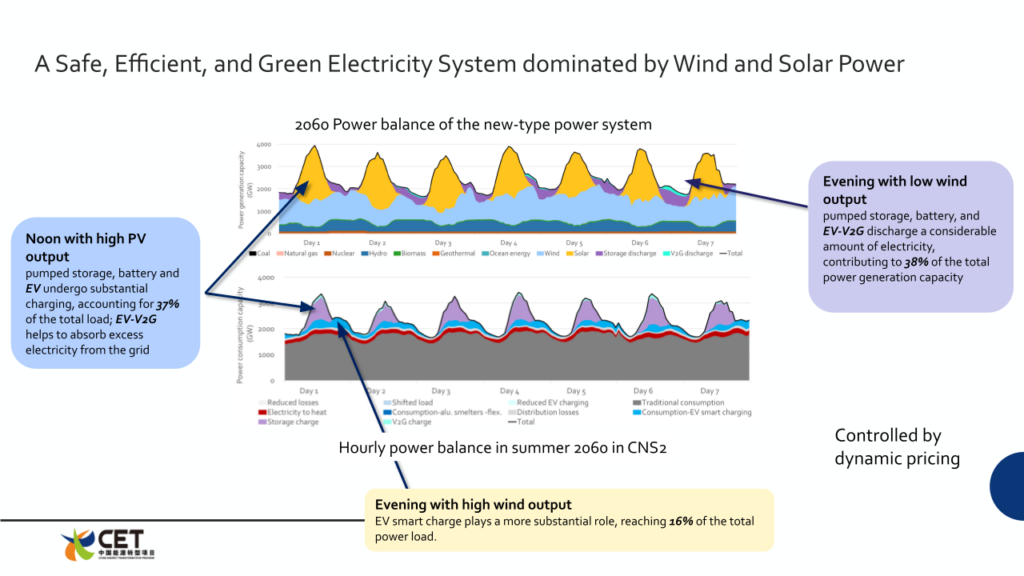

An energy system that relies on solar and wind power as main suppliers of power requires special flexibility measures to match production and demand.

The figure below shows a modelled example of an hourly electricity balance in a week in the summer of 2060 under our more ambitious scenario of achieving carbon neutrality before 2055.

The top panel shows electricity production on the supply side. In the daytime solar power (yellow) dominates the production of electricity, while wind power plants (light blue) have a more stable output throughout the 24-hour period.

In the evening and at night, electricity storage is discharged (purple) and hydropower production (dark blue) is higher than in the daytime.

The lower panel shows electricity use on the demand side. Storage (purple) is charged in the daytime and electric vehicle (EV) smart charging (blue) provides flexibility throughout the week.

{kind=link}

As a backup, vehicle-to-grid supply plays an important role – not necessarily as a significant energy provider but as a last-resort capacity that can be activated if necessary, when wind and solar output is low. This solution is a cheap and efficient way to ensure sufficient capacity in the power system.

Before 2055, coal power plants could be equally reliable and affordable providers of capacity for the power system, even though they would not generate much electricity on average, as mentioned earlier.

This way of creating flexibility might seem complicated to manage in terms of daily dispatch (the process of managing supply and demand). However, an efficient and well-functioning electricity market, including consumers and producers, can do the job.

Removing the barriers to electricity trading among provinces and constructing a unified national electricity market would be a key enabler of this.

§ Visions for the future

The scenarios from our China Energy Transformation Outlook give a range of quantified visions of the long-term future in a net-zero energy system.

Our detailed model of the power system and other energy end-use sectors make it possible to link the development of this new energy system with policy measures that could bring about this transformation.

One key insight from our work relates to the timing of the different phases of China’s energy transformation, mentioned above. Our modelling suggests that successful coordination of these phases will be crucial, in order to maintain energy security while avoiding unnecessary investments in energy infrastructure.

Other key enablers in our scenarios are the investments needed to expand the electricity grid, the development of a national electricity market and support for energy system flexibility.

Even with the best visions, and insights from pathways such as ours, there will be many challenges and barriers ahead to overcome if China is to reach its 2060 goal.

Our scenarios show, however, that there are feasible and cost-efficient pathways which can be implemented without waiting for new technological breakthroughs.