Analysis: China’s emissions set to fall in 2024 after record growth in clean energy

China’s carbon dioxide (CO2) emissions are set to fall in 2024 and could be facing structural decline, due to record growth in the installation of new low-carbon energy sources.

The new analysis for Carbon Brief, based on official figures and commercial data, shows China’s CO2 emissions continuing to rebound from the nation’s “zero-Covid” period, rising by an estimated 4.7% year-on-year in the third quarter of 2023.

The strongest growth was in oil demand and other sectors that had been affected by pandemic policies, until the lifting of zero-Covid controls at the end of 2022.

Other key findings from the analysis include:

- China has been seeing a boom in manufacturing, which has offset a contraction in demand for carbon-intensive steel and cement due to the ongoing real-estate slump.

- The emissions rebound in 2023 has been accompanied by record installations of low-carbon electricity generating capacity, particularly wind and solar.

- Hydro generation is set to rebound from record lows due to drought in 2022-23.

- China’s economic recovery from Covid has been muted. To date, it has not repeated previous rounds of major infrastructure expansion after economic shocks.

- There has been a surge of investment in manufacturing capacity, particularly for low-carbon technologies, including solar, electric vehicles and batteries.

- This is creating an increasingly important interest group in China, which could affect the country’s approach to domestic and international climate politics.

- On the other hand, coal power capacity continues to expand, setting the scene for a showdown between the country’s traditional and newly emerging interest groups.

Taken together, these factors all but guarantee a decline in China’s CO2 emissions in 2024.

If coal interests fail to stall the expansion of China’s wind and solar capacity, then low-carbon energy growth would be sufficient to cover rising electricity demand beyond 2024. This would push fossil fuel use – and emissions – into an extended period of structural decline.

- Emissions are set to fall in 2024

- Why emissions grew in Q3 of 2023

- Coal expansion threatens China’s international commitments for 2025

- Solar, wind and hydropower set to surge in 2024

- Continued clean-power growth can peak emissions in 2024

- Why did clean energy investments surge during and after Covid?

- What comes next for China’s emissions peak and decline

- Data sources

§ Emissions are set to fall in 2024

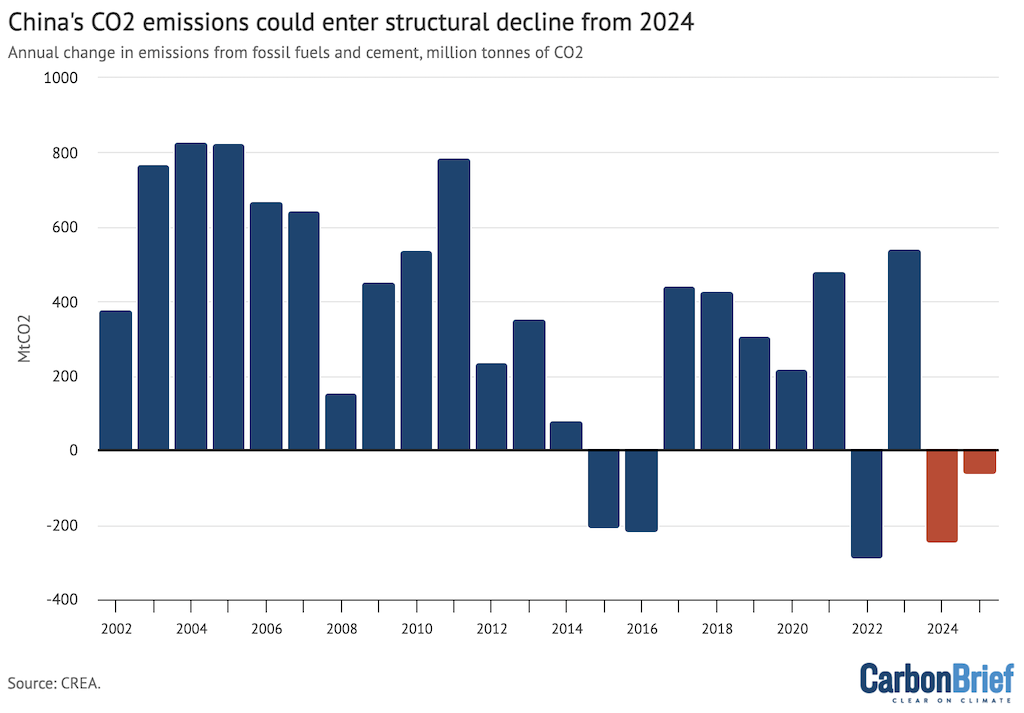

China’s CO2 emissions have seen explosive growth over recent decades, pausing only for brief periods due to cyclical shocks.

Over the past 20 years, its annual emissions from fossil fuels and cement have climbed quickly almost every year – as shown in the figure below – interrupted only by the economic slowdown of 2015-16 and the impact of zero-Covid restrictions in 2022.

While CO2 is rebounding in 2023 from zero-Covid lows (see: Why emissions grew in Q3 of 2023), there have also been record additions of low-carbon capacity, setting up a surge in electricity generation next year. (See: Solar, wind and hydropower set to surge in 2024.)

Combined with a rebound in hydro output following a series of droughts, these record additions are all but guaranteed to push fossil-fuel electricity generation and CO2 emissions into decline in 2024, as shown in the figure below.

{kind=link}

Moreover, with the power sector being China’s second-largest emitter and with other major sectors, such as cement and steel, already seeing CO2 falling, this drop in power-sector emissions could drive a sustained, structural emissions decline for the country as a whole.

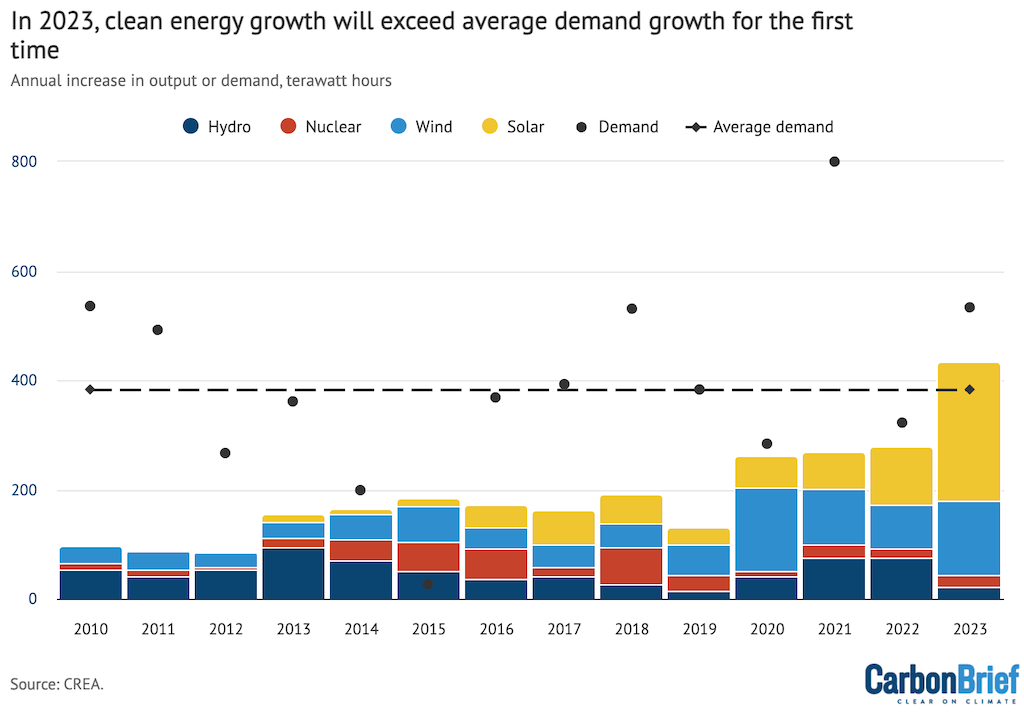

This is because – for the first time – the rate of low-carbon energy expansion is now sufficient to not only meet, but exceed the average annual increase in China’s demand for electricity overall. (See: Continued clean power growth can peak emissions in 2024.)

If this pace is maintained, or accelerated, it would mean that China’s electricity generation from fossil fuels would enter a period of structural decline – which would also be a first.

Moreover, this structural decline could come about despite the new wave of coal plant permitting and construction in the country. (See: Coal expansion threatens China’s international commitments for 2025.)

In addition, record additions of low-carbon energy deployment have been accompanied by rapid expansion in related manufacturing capacity. (See: Why did clean energy investments surge during and after Covid?)

This could create tension with traditional interests in the country’s coal industry, yet it also boosts the economic and political case for China to continue supporting low-carbon growth, both at home and abroad. (See: What comes next for China’s emissions peak and decline.)

§ Why emissions grew in Q3 of 2023

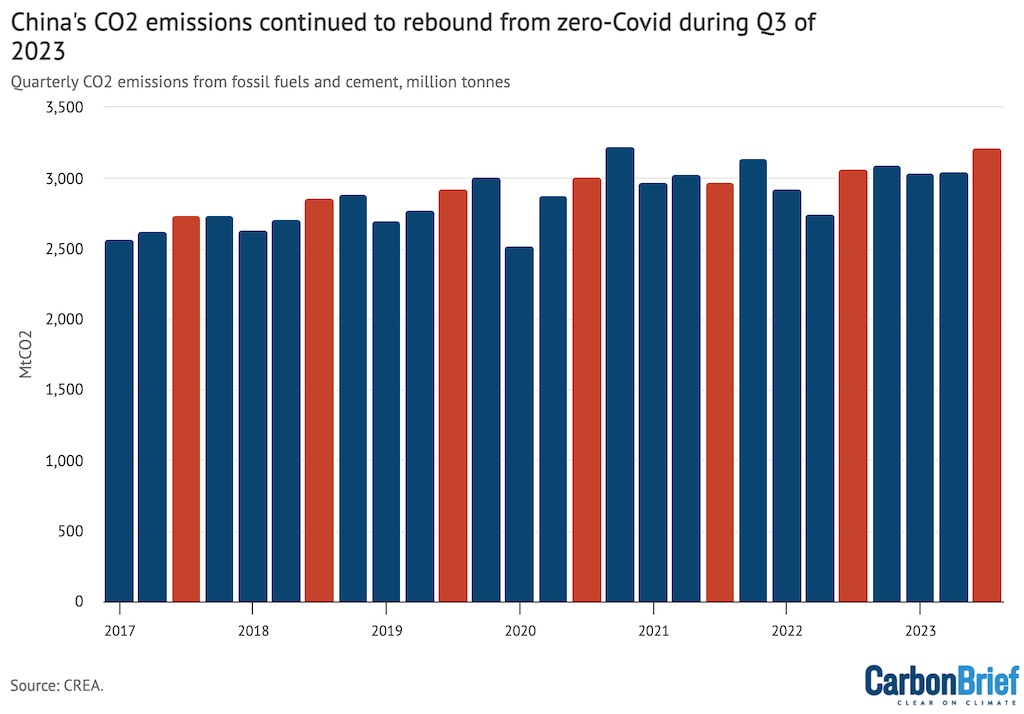

China’s CO2 emissions continued to rebound in the third quarter of 2023, increasing an estimated 4.7% year-on-year, but slowing to 1% in September.

This follows rapid growth in the first and second quarters of the year, after the same periods in 2022 had seen emissions decline by record amounts.

China’s quarterly CO2 emissions from energy use and cement production are shown in the figure below, with the third quarter of each year highlighted in red.

{kind=link}

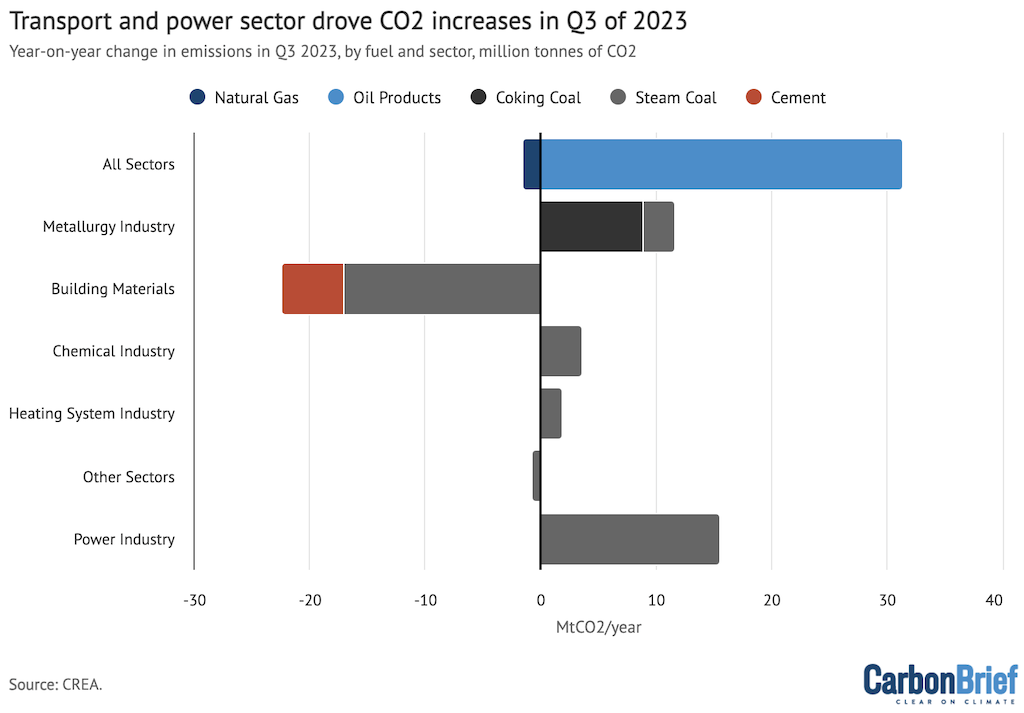

The reasons for the emissions rebound this year are predictable. Most significantly and obviously, oil demand has risen from zero-Covid lows, following almost three years of pandemic controls.

Oil consumption is now approaching the pre-Covid trendline and does not yet show any sign of abating, increasing by an estimated 19% year-on-year in the third quarter. This is shown by the large light blue bar at the top of the figure below.

Electricity demand also rebounded from Covid lows in sectors that had been affected by pandemic controls, making power-sector coal use the second-largest driver of rising emissions in the third quarter of the year (the lowest grey bar).

The increase in power-sector demand happened almost entirely in July, before hydropower generation began to rebound from historic lows caused by low rains in 2022 and early 2023.

{kind=link}

Coal use outside the power sector fell (grey chunks), due to a major drop in building materials driven by the ongoing contraction of real-estate construction and construction of associated infrastructure. This is also reflected in the drop for cement emissions (red).

Other uses of coal increased, particularly the use of coking coal (black chunks). The increase in coal use for steelmaking was larger than the increase in steel output, indicating a shift from electric arc to coal-based steel production.

Investment growth – for example, investment in electrical machinery manufacturing grew 38% year-on-year and investment in railways grew 22% – has supported demand for energy-intensive commodities, despite an ongoing contraction in real estate, generally the main user of metals.

Gas use continued to fall (dark blue), reflecting a drop in demand and a shift from gas to electricity and coal due to high prices.

§ Coal expansion threatens China’s international commitments for 2025

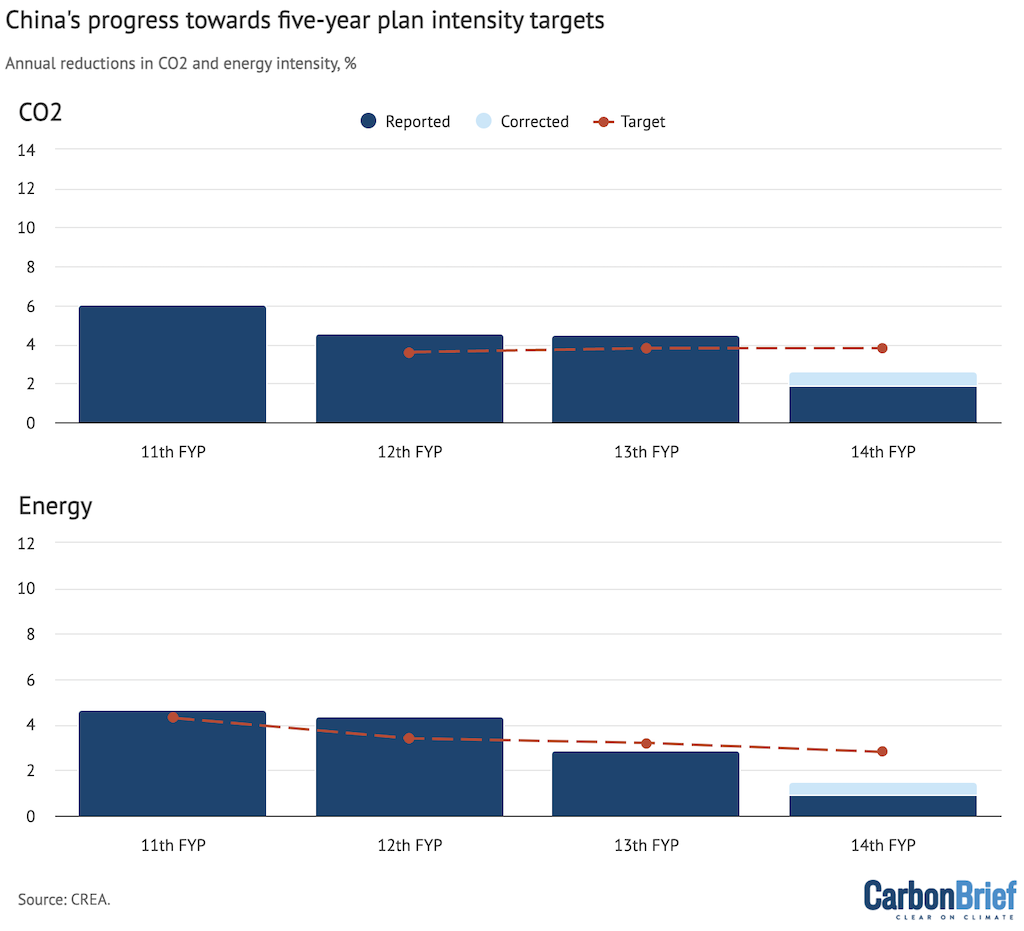

The pattern of economic growth in China, both during and after the Covid-19 pandemic, was highly energy- and carbon-intensive. This has put China off track against the CO2 and energy intensity targets – aimed at reducing CO2 and energy use per unit of GDP – that it promised in its updated climate pledge (nationally determined contribution, NDC) in 2021.

This would mark a departure from previous progress, with China having exceeded its energy and CO2 intensity targets during the 11th (2006-2010) and 12th (2011-2015) five-year plan periods, as shown in the figure below.

The slowdown in progress on energy intensity began already at the end of the 13th five-year plan period (2016-2020), resulting in that target being missed.

{kind=link}

The coming surge of low-carbon energy would put the country on track for the CO2 intensity target, if similar levels are added next year.

The energy intensity target, in contrast, will not be met on current trends. Only a sharp shift to consumption-driven growth – which the government says it prefers, but has found the required measures hard to implement – could allow this target to be hit.

Permitting of new coal power plants continued, with at least another 25GW given the go-ahead in the third quarter, based on a compilation of permits reported by Polaris Network.

The resurgence of coal-plant construction contradicts a policy pledge that China’s president Xi Jinping personally announced. Xi pledged to “strictly control new coal-fired power generation projects” in China in 2021–25.

This pledge was made in the Leaders Summit on Climate in April 2021 and consequently added to China’s NDC, just months before the current wave in coal power plant permitting and construction began.

The State Council Development Research Center recently projected that China’s coal power capacity should peak at 1,370GW in 2030, up from 1,141GW at the end of June.

As 136GW was already under construction at the end of June, another 99GW had already been permitted, and a further 25GW has been permitted since, realising this projected peak would mean stopping new permits immediately.

Alternatively, retirements of existing capacity would have to be accelerated significantly, or some already permitted projects would have to be cancelled or shelved.

§ Solar, wind and hydropower set to surge in 2024

While emissions have climbed in 2023, it has also seen a historic expansion of low-carbon energy installations. The most striking growth has been in solar power, where expected installations in 2023 – some 210 gigawatts (GW) – are twice the total installed capacity of solar power in the US and four times what China added in 2020.

The newly installed solar, wind, hydro and nuclear capacity added in 2023 alone will generate an estimated 423 terawatt hours (TWh) per year, equal to the total electricity consumption of France.

About half of the solar panels added this year will be installed on rooftops, largely driven by China’s “whole county solar” model, where a single auction is carried out to cover a targeted share of the rooftops in a county with solar panels in one fell swoop.

Under this model, the developer negotiates with building owners and arranges contracts with the grid, financing, procurement, contracting and installations. This model – which could be described as centralised development of distributed solar – has enabled rooftop solar deployment at a vast scale.

The other half of solar installations are set to be in large utility-scale developments, particularly in the gigawatt-scale “clean energy bases” in western and northern China.

All in all, 210GW of solar, 70GW of wind, 7GW hydro and 3GW of nuclear are expected to be added in China this year. This is shown in the table below, along with expected electricity generation assuming newly added capacity performs in line with the existing fleet.

Expected capacity additions in 2023 and added annual generation| Source | GW | Average utilisation | TWh |

|---|---|---|---|

| Solar | 210 | 13.6% | 251 |

| Wind | 65 | 23.0% | 130 |

| Nuclear | 3 | 83.4% | 21 |

| Hydro | 7 | 36.7% | 21 |

| Total | 284 | 17.0% | 423 |

In addition to the electricity generated by this newly added capacity, China is likely to see a large year-on-year increase in output from its massive hydropower fleet in 2024.

The utilisation of this fleet plumbed historical lows from August 2022 until July 2023, as a result of record droughts and heatwaves in summer 2022, followed by low rainfall into 2023.

The year-on-year drop in power generation was compounded as hydropower operators were conserving water in the spring and early summer of 2023, building up the water levels in their reservoirs for the peak demand season in August.

(This behaviour is clear in CREA analysis of hydropower generation data and water levels at 13 major hydropower reservoirs across China, reported by Wind Financial Terminal, showing water levels approaching historical highs while output remained low until July.)

This was in stark contrast with 2022, when spring and early summer had good rains and hydropower was generating at very high rates.

In addition to the electricity generated by this newly added capacity, China is likely to see a large year-on-year increase in output from its massive hydropower fleet in 2024.

The utilisation of this fleet plumbed historical lows from August 2022 until July 2023, as a result of record droughts and heatwaves in summer 2022, followed by low rainfall into 2023.

The year-on-year drop in power generation was compounded as hydropower operators were conserving water in the spring and early summer of 2023, building up the water levels in their reservoirs for the peak demand season in August.

(This behaviour is clear in CREA analysis of hydropower generation data and water levels at 13 major hydropower reservoirs across China, reported by Wind Financial Terminal, showing water levels approaching historical highs while output remained low until July.)

This was in stark contrast with 2022, when spring and early summer had good rains and hydropower was generating at very high rates.

In China’s rigidly regulated power system, hydropower operators do not have an economic incentive to time their output to the peak demand season. However, after the electricity shortages of summer 2022, administrative intervention appears to have replaced economic incentives and compelled generators to ensure high reservoir levels.

Now water levels in reservoirs have climbed up to or above their seasonal averages, based on data from Wind Financial Terminal. Long-term weather forecasts point to above-average rains lasting until February, the end of the forecast period, consistent with predictions for the current El Nino.

If these forecasts hold out, hydropower utilisation will not only recover but come in above historical averages in 2024. Meanwhile, another 29GW of hydropower has been added from the beginning of 2022 to September 2023, marking a 7% increase in capacity.

The hydropower generation rebound had already begun in August-September and will continue through this year. However, electricity demand growth at the end of last year was very weak due to strict Covid lockdowns, so emissions are unlikely to fall year-on-year.

Total CO2 emissions fell 4% from the last quarter of 2020 to the last quarter of 2022, setting up a very low base of comparison for the last quarter of this year.

§ Continued clean-power growth can peak emissions in 2024

Given the low-carbon electricity capacity already installed this year – and the outlook for hydropower generation – a drop in power-sector emissions in 2024 is essentially locked in, barring a major acceleration in electricity demand growth.

From 2025 onwards, the development of power-sector emissions depends on whether low-carbon energy additions are maintained or accelerated.

Looking at the added annual generation from low-carbon energy installations in 2023, the total comes out to more than the average annual increase in China’s power demand, for the first time, marking a potential inflection point.

At this point, the growth of low-carbon electricity (columns in the chart below) would outweigh the overall growth of electricity demand (dots). As a result, the amount of electricity generated using fossil fuels – and the associated emissions – would decline.

{kind=link}

As long as low-carbon energy installations are maintained at the projected 2023 level, the growth in low-carbon power generation would enable China to peak and decline coal use in the power sector imminently, with 2023 remaining the peak year.

How will power-sector emissions develop if the 2023 level of low-carbon energy additions is maintained?

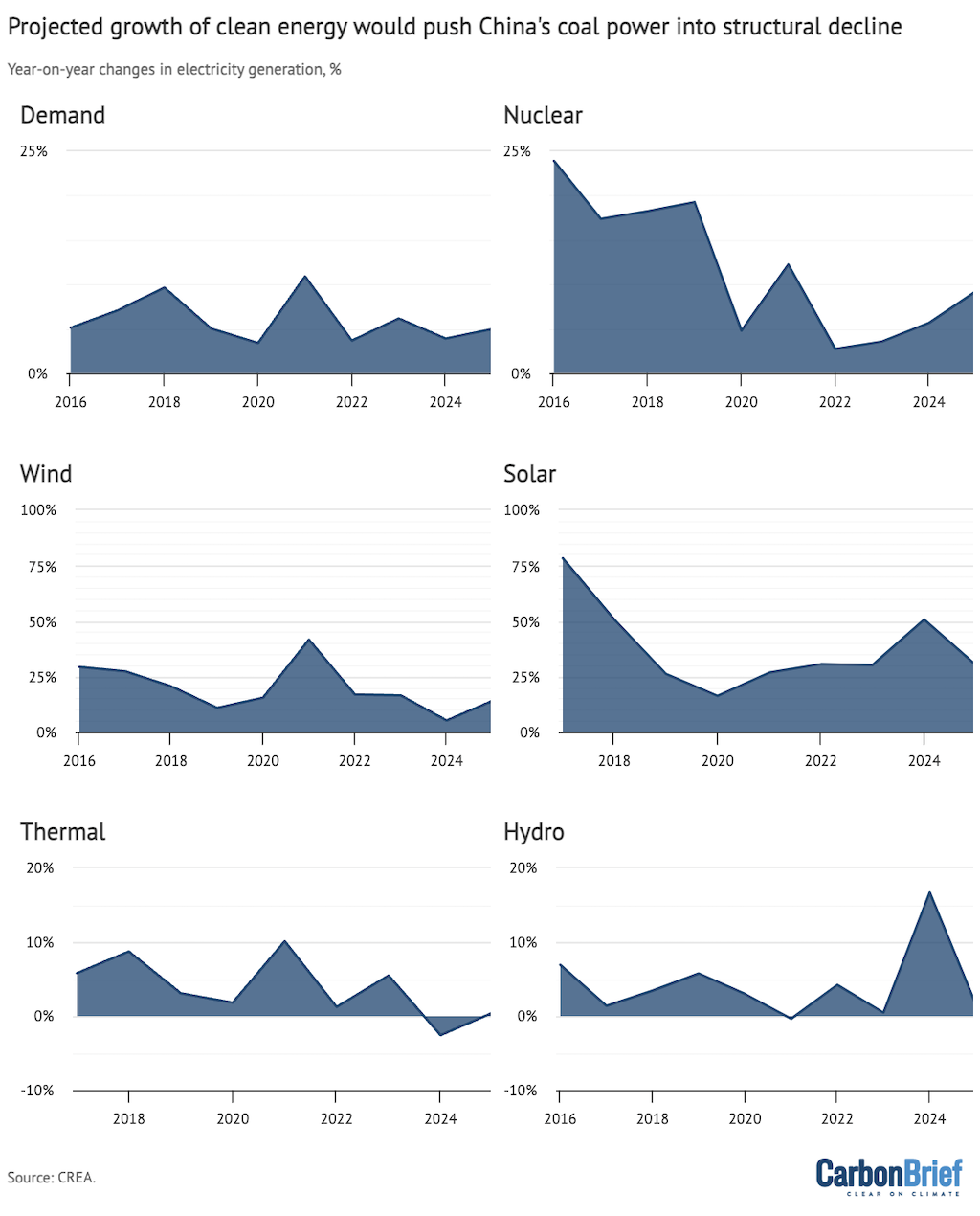

A simple projection – assuming that electricity demand follows its historical trend of rising 5% per year and hydropower utilisation returns to historical averages – points to a significant drop in fossil fuel-based (thermal) power generation in the spring and summer of 2024, shown by the bottom left segment in the chart below, and zero growth thereafter.

If China’s current and expected economic slowdown results in slower electricity demand growth – or non-fossil energy additions accelerate further – power generation from fossil fuels will continue to fall, rather than stabilise.

Under these assumptions, hydropower generation would see steep increases already in October 2023 – January 2024, but power generation from fossil fuels still climbs year-on-year, due to the low base set under the zero-Covid policy.

A return to average demand growth rates after the post-Covid rebound, (top left), continued strong growth in solar (centre right) and wind (centre left) output, combined with rebounding hydropower output (bottom right), would push fossil-fuel power generation down from February 2024 onwards (bottom left). This would mean fossil fuel-fired electricity generation falling 3% in 2024 and remaining at similarly reduced levels in 2025.

{kind=link}

Moreover, rapid electrification has meant that almost all of the recent growth in China’s CO2 emissions has taken place in the power sector.

Therefore, when power-sector emissions peak, total emissions are likely to follow, as falling coal use outside the power sector balances out increases in oil and possibly gas demand, which are also mitigated by electrification.

§ Why did clean energy investments surge during and after Covid?

China’s output of solar cells is set to exceed 600GW this year, up from 375GW last year and enough to produce 500GW of solar panels. For comparison, only 240GW of panels were installed globally last year.

The output of batteries in China will reach 800 gigawatt hours (GWh), up from 550GWh last year and enough to power 20m electric vehicles (EVs).

Electric vehicle output exceeded 8m units over the 12 months to September, representing more than 30% of all vehicles produced in China. The share of EVs in all vehicles sold in China is also on track to reach 30% in 2023, while production for the calendar year is set to reach 9m vehicles.

This is only the beginning of the industry’s expansion plans. By 2025, solar-panel production capacity is expected to break 1,000GW (1 terawatt, TW), and battery production capacity to reach 3,000GWh.

What is causing this surge?

The announcement of the 2060 carbon neutrality target provided the political signal, but wider macroeconomic conditions have delivered low-carbon capacity growth far in excess of policymakers’ targets and expectations, with this year’s solar and wind installation target met by September and the market share of EVs already well ahead of the 20% target for 2025.

The clampdown on the highly leveraged real-estate sector, starting in 2020, led to a steep drop in the demand for land, commodities, labour and credit for apartments and associated infrastructure. This left a hole in the finances of local governments – which rely on land sales for a lot of their revenue – and hit economic growth rates.

Local governments were, thus, searching for alternative investment opportunities to drive economic growth. Yet, at the same time, their investment spending was under scrutiny due to debt concerns. China’s high-level environmental and industrial policy goals made cleantech one of the acceptable sectors for their investment.

At the same time, the government made it easier for private-sector companies to raise money on the financial markets and from banks, as part of measures to stimulate the economy during the pandemic.

The low-carbon energy sector, in contrast with the fossil fuel and traditional heavy industries, is largely made up of private companies. Access to credit had earlier been a major bottleneck for them in a financial system that has heavily favoured state-owned firms.

As a result, much of the bank lending and investment that previously went into real estate is now flowing to manufacturing – largely cleantech manufacturing – as well as to cleantech deployment.

Local government enthusiasm for attracting investments to their regions meant that they often also offered major direct or indirect subsidies. Reportedly, it is common for local governments to build an entire factory and associated infrastructure, with the private company going on to occupy the site only covering the cost of machinery and operations.

All of this happened at a time when falling costs driven by technological learning and subsidies resulted in many low-carbon energy technologies becoming economically competitive against fossil fuels.

China’s policymakers had favoured “green” investments previously, as in the 2009 stimulus package launched in response to the global financial crisis. Yet the sector had been too small to absorb the huge amount of credit mobilised as a part of China’s stimulus cycles. After experiencing extremely rapid growth since 2020, this has changed.

The construction of low-carbon energy manufacturing capacity, production of low-carbon energy equipment and construction of railways have been significant drivers of commodity demand this year, as the only areas of investment showing substantial growth.

This demand explains, among other things, why China’s steel output has continued to grow despite the ongoing contraction in real-estate construction.

Conversely, the precipitous drop in demand for commodities from the real estate and conventional infrastructure sectors explains why the breakneck expansion of low-carbon energy sectors – and their commodity demand – has not resulted in a spike in prices.

The unprecedented investment in low-carbon technology manufacturing supply chains also means that China has, in effect, placed a major economic and financial bet on the success of the global energy transition, which could affect its diplomatic positioning.

§ What comes next for China’s emissions peak and decline

Now that low-carbon energy expansion has reached the scale needed to start driving down China’s emissions, the most important question is: will its growth continue?

China’s low-carbon energy boom resulted from the confluence of numerous factors. There was – and is – clear political commitment and direction. The contraction of the real-estate market provided a push and an opportunity for the redirection of capital and investments into the renewable energy sector.

Technological learning and aggressive industrial policy improved quality and cut costs to the point where the market for low-carbon energy technologies started to expand rapidly.

It is also clear that the wave of manufacturing investment has resulted in significant overcapacity in the production of solar panels, batteries and EVs, among others, though the scale of this excess depends on the pace of the global energy transition.

This overcapacity is likely to be resolved – as in previous rounds of expansion – through consolidations and outright failures of individual players. Meanwhile, however, it will continue to depress the prices of low-carbon energy equipment.

Politically, the major challenge will only come when low-carbon energy begins to substantially cut into the demand for coal and coal-fired power.

This shift threatens the interests of the coal industry and local governments with a high exposure to the coal sector. These stakeholders could be expected to resist the transition, raising concerns about potential roadblocks.

When contraction in demand and capacity additions resulted in overcapacity in coal-fired power around 2015, coal power interests successfully argued that low-carbon energy deployment had been too fast.

As a result, the rate of low-carbon energy capacity additions slid down from 2015 until 2019, as seen in the figure above, making more space for excess coal capacity to generate power.

A similar balancing act could come into play once again, as coal and low-carbon generating capacity both continue to expand, competing to meet limited rises in demand.

The Chinese government and its advisers have argued that new coal power plants will not result in a surge in emissions, as they will be used for flexible operation at low utilisation.

China’s climate targets do not yet reflect this belief, however. Its combination of intensity and low-carbon deployment targets would allow emissions to increase by another 10-15% from 2022 levels and only peak at the end of this decade.

If the government wanted to more firmly cement the low utilisation of newly built coal plants, it could do so by moving towards an absolute cap on power-sector emissions under its emissions trading system – or by setting a limit on China’s total CO2 emissions.

As the government weighs these decisions, it is faced with a dramatically larger set of economic drivers and interests in the low-carbon energy sector, as compared with 2015.

These conditions could offer the motivation for policymakers to push a faster domestic transition away from fossil fuels. They also mean that China has an increasingly significant financial stake in the success of the low-carbon transition worldwide.

§ Data sources

Data for the analysis was compiled from the National Bureau of Statistics of China, National Energy Administration of China, China Electricity Council and China Customs official data releases, and from WIND Information, an industry data provider.

Power sector coal consumption was projected based on power generation, to avoid the issue with official coal consumption numbers affecting 2022–23 data. September 2023 data on apparent coal consumption was not available at the time of publication, so coal consumption in different sectors was projected based on the output of relevant industrial products – for example, coke for the consumption of coking coal; cement and glass for building materials industry. Coal consumption for heating was projected based on population-weighted average heating degree days calculated from NCEP gridded daily weather data.

When data was available from multiple sources, different sources were cross-referenced and official sources used when possible, adjusting total consumption to match the consumption growth and changes in the energy mix reported by the National Bureau of Statistics.

CO2 emissions estimates are based on National Bureau of Statistics default calorific values of fuels and IPCC default emissions factors. Cement CO2 emissions factor is based on 2018 data.

For oil consumption, apparent consumption is calculated from refinery throughput, with net exports of oil products subtracted.