The Carbon Brief Profile: South Africa

In the fourth article in a series on how key emitters are responding to climate change, Carbon Brief looks at South Africa’s heavy dependence on coal and expanding effort to develop renewables.

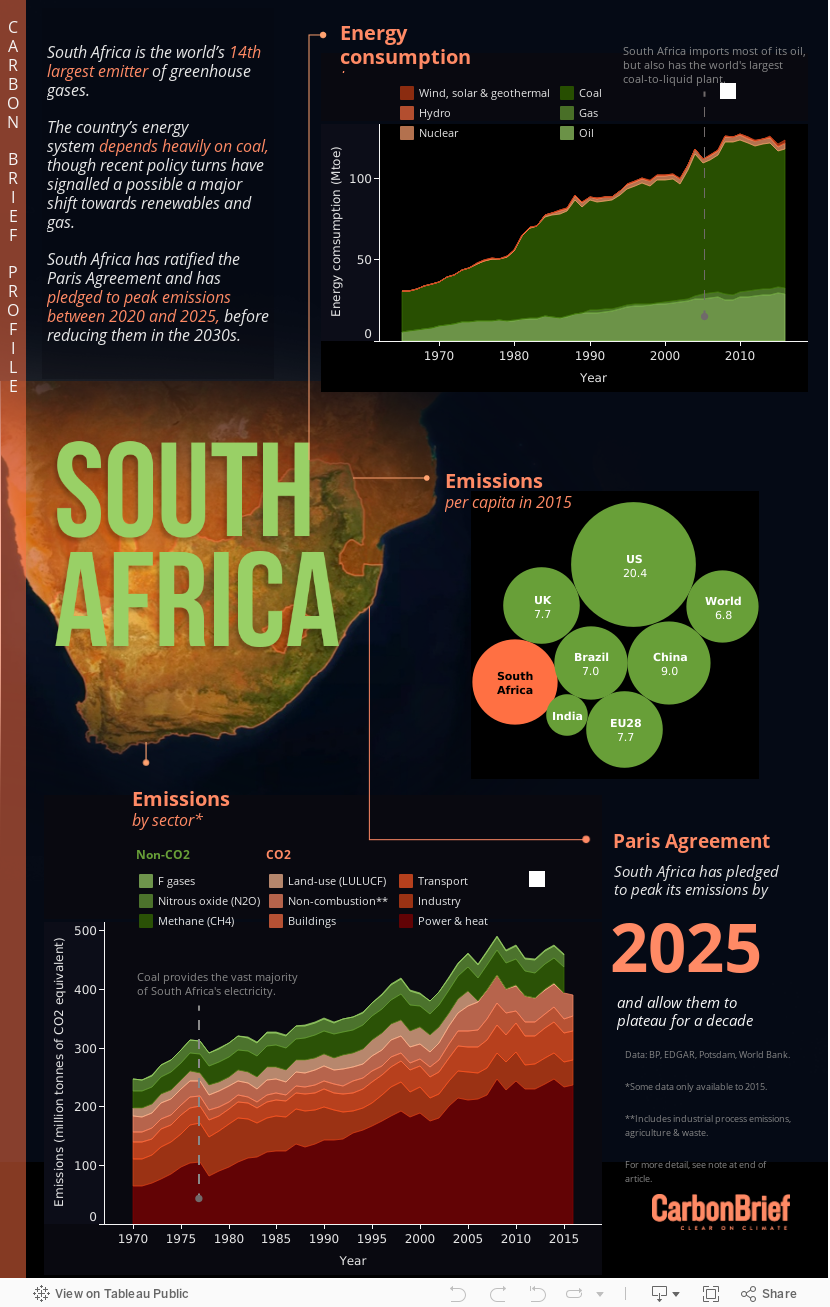

South Africa is the world’s 14th largest emitter of greenhouse gases (GHGs). Its CO2 emissions are principally due to a heavy reliance on coal.

However, a recently released draft electricity plan proposes a significant shift away from the fuel, towards gas and renewables. While coal would continue to play a role for decades, the plan would see no new plants built after 2030 and four-fifths of capacity closed by 2050.

South Africa has pledged to peak its emissions between 2020 and 2025, allowing them to plateau for roughly a decade before they start to fall.

§ Politics

South Africa is one of Africa’s most industrialised countries and has the continent’s second largest economy after Nigeria. In the decades since apartheid ended in the early 1990s, its economy has more than tripled in size, but faltered in recent years. It currently ranks 32nd in the world.

President Cyril Ramaphosa, leader of the governing African National Congress (ANC) party, was elected by parliament in February 2018. President Jacob Zuma, his predecessor of the same party, had been in office for 9 years. He resigned the day before Ramaphosa’s election while facing his ninth vote of no confidence.

South Africa’s climate efforts have been criticised, particularly due to its continuing heavy reliance on coal. While Zuma vocally supported climate action, his government was accused of delaying the development of policies to cut emissions.

{kind=link}

{kind=link}

Deputy President Cyril Ramaphosa joined flanked by Ministers Rob Davies, Jeff Radebe, Ebrahim Patel and Melusi Gigaba addressing a media conference at the end of his engagements at the World Economic Forum 2018 Annual Meeting in Davos, Switzerland. 25 Jan 2018. Credit: Elmond Jiyane/GCIS.

Ramaphosa’s cabinet has recently announced plans for a major shift away from coal and expansion of renewables. He also told CNN that Cape Town’s recent drought showed climate change was a reality, adding:

“If people around the world ever thought climate change is just a fable‚ we in South Africa are now seeing the real effects of climate change. We are facing a real, total disaster in Cape Town, which is going to affect more than four million people.”

The country will return to the polls by summer 2019 to elect a new National Assembly, which will in turn determine the next president. Current polls favour the ruling ANC party, which has been in power since the end of apartheid and the election of Nelson Mandela in 1994. The centrist Democratic Alliance (DA) party – the official opposition – received 22% of votes in the last election in 2014, compared to the ANC’s 62%.

In 2011, South Africa hosted the 17th formal meeting of the UNFCCC (United Nations Framework Convention on Climate Change) in Durban. Here, countries agreed to establish a new universal and legally binding climate treaty in 2015 for the post-2020 period. This, ultimately, led to the 2015 Paris Agreement. The UNFCCC has called the Durban conference a “turning point” in international climate negotiations.

Polls show 45% of South Africans consider climate change to be a very serious problem, in the middle of the range for the world’s major economies.

§ Paris pledge

South Africa is part of four negotiating blocs at international climate negotiations. These include BASIC, a coalition of four major emerging economies (along with Brazil, India and China); the African Group; the G77 + China; and the Coalition for Rainforest Nations (CfRN).

The country’s GHG emissions in 2015 sat at 460m tonnes of CO2 equivalent (MtCO2e), according to data compiled by the Potsdam Institute for Climate Impact Research (PIK), putting it in 14th place worldwide. Emissions rose steadily for much of the past 50 years, growing from around 250MtCO2e in 1970 to a peak of 490MtCO2e in 2008. They have since declined – unevenly – as the economy faltered.

South Africa submitted its climate pledge, or “nationally determined contribution” (NDC), for the Paris climate talks on 25 September 2015. This pledges a “peak, plateau and decline” approach, whereby emissions would peak between 2020 and 2025, plateau for roughly a decade, and then start to fall. Emissions during 2020-2025 would be between 398-614MtCO2e, it says, including land use and all sectors of the economy. This “plateau” would translate to a 14-75% rise above 1990 levels.

{kind=link}

{kind=link}

The Minister of Environmental Affairs of South Africa Bomo Edith Edna Molewa signs the Paris Agreement on climate change at United Nations headquarters in New York. 22 April, 2016. Credit: Xinhua / Alamy Stock Photo.

South Africa says its pledge is an “equitable contribution” to global mitigation efforts, given its emissions to date and its national circumstances. It points to its “overriding priorities to eliminate poverty and eradicate inequality” and notes that the country is “facing acute energy challenges that hamper economic development”. Its “fairly apportioned” share of the global carbon budget would exceed the upper limit of its trajectory range, it adds.

However, Climate Action Tracker (CAT), an independent scientific analysis produced by three research organisations tracking climate action, rates South Africa’s NDC as “highly insufficient”. This means its pledge is outside a “fair share” of the emissions cuts needed to meet the goals of the Paris Agreement, and “not at all” consistent with limiting global warming to less than 2C or 1.5C. If all governments had similar targets, global temperature rise would likely reach 3-4C by 2100, says CAT.

Under its currently implemented policies and assuming continued low economic growth, South Africa will reach the upper end of its 2030 emission reduction targets in 2020 and 2025, says CAT. By 2030, emissions would breach its Paris pledge, with emissions around 27MtCO2e higher than the upper end of the 2030 target.

Overall, CAT projects that South Africa’s emissions will increase to 90% above 1990 levels by 2030, excluding land use and forestry (land use, land-use change and forestry, or “LULUCF”). Higher economic growth than anticipated could further increase this.

South Africa’s per capita emissions stood at 9.5 tonnes of CO2 equivalent (tCO2e) in 2015, around half of US per capita emissions but well above the world average of 6.8tCO2e.

Climate Transparency, a “global partnership with a shared mission to stimulate a ‘race to the top’ in G20 climate action”, rates (pdf) South Africa’s climate policies predominantly as “medium” in terms of consistency with the Paris Agreement.

§ Energy policy

South Africa has seen considerable energy sector challenges in recent years. For example, shortages mean it has had to repeatedly curb electricity supply in some areas – known as “load shedding” – to protect the power system from total blackout.

In addition, national power supplier Eskom has experienced major financial problems, which the treasury has described as the single biggest risk to the South African economy. Eskom is responsible for 95% of electricity supply, operates the country’s grid and owns most of its coal-fired power plants. Cost and time overruns at two large coal plants it is building are a major cause of its financial problems.

“Worrying” allegations of financial irregularities and governance concerns have also surfaced at Eskom, according to a paper released in February 2018 by the country’s independent National Planning Commission (NPC).

In August 2018, South Africa’s government released a long-awaited draft update to the country’s Integrated Resource Plan (2018 draft IRP). This sets out the government’s plans for electricity capacity expansion up to 2030, based on its analysis of the “least cost” option.

The current electricity plan, known as the 2010 IRP, was finalised in 2011 as part of the broader Integrated Energy Plan (IEP), which covers all energy including liquid fuels. As a “living plan”, it was supposed to be updated regularly, but the cabinet failed to adopt either of two proposed drafts in 2013 and 2016. Importantly, the plan has legislative power, meaning the government is bound by it when deciding what new power can be procured.

Until a new draft is adopted, the 2010 version remains official policy. It contains 2030 targets for all technologies, including a large expansion of nuclear and continued growth for coal. The plan also sets an overall cap on emissions from electricity generation, from 2025 onwards.

In contrast, the draft 2018 update puts the greatest emphasis on new renewables and gas in its “least-cost plan” to 2030. It considerably reduces plans for new coal and excludes new nuclear. However, it still indicates nuclear and “clean” coal could be considered in the longer term up to 2050.

The revised plan, if adopted, “would mark a major shift in energy policy…remarkable for a coal-dominated country like South Africa,” according to CAT. However, others have warned its continued reliance on a “coal-based business model” is not financially viable and will require large bailouts into the future.

Implementation of this plan could bring South Africa close to being within the emissions range of its Paris target for 2030, CAT says. However, more ambitious plans would still be needed to meet the pledge, it adds.

The draft IRP has now gone to public consultation for 60 days, ending in November. While the cabinet has not given a date for final adoption, energy minister Jeff Radebe has said he hopes it will be soon after the comment period. The update faces opposition from some unions and the nuclear industry. Unusually – and significantly – it is broadly supported by heavy industry, which favours an ambitious shift towards cleaner energy.

§ Coal

South Africa is the world’s 7th largest coal producer. Its sizeable reserves have led coal to form the backbone of its economy for well over a century. However, cheap, easily accessible coal reserves could now be nearing an end. There’s also rising awareness of the large health impacts of coal power in the country.

Coal has provided the vast majority of South Africa’s electricity for decades, as the chart below shows. In 2017, coal produced 88% of the country’s electricity.

BP Statistical Review of World Energy 2018HighchartsSouth Africa’s reliance on coal means around 80% its emissions come from energy supply, according to the NPC.

As of July 2018, South Africa has 42GW of operating coal plants, the seventh largest fleet in the world, according to the Global Coal Plant Tracker. It also has 6GW of new coal-fired plants under construction and a further 3GW in the planning stage.

The existing coal generation fleet is ageing and has experienced a number of reliability issues. Two new large-scale coal power plants currently under construction – Medupi and Kusile – have also seen major cost and time overruns. These two coal plants are set to provide 4.8GW each, some of which is already operating.

Cost increases, energy security risks, export demand risks and low local demand growth mean the coal sector is facing significant challenges, says a 2018 report from the Energy Research Centre (ERC) at the University of Cape Town. It adds:

“These are already having profound implications for South African electricity consumers. For example, Eskom’s primary energy costs have increased by 300% in real terms over the past 20 years.”

Coal project cost increases and overruns have led to rapidly increasing electricity prices, the report adds, in turn stagnating demand for electricity. Electricity demand has been declining for years in South Africa and currently sits at 2007 levels. Significantly, this is some 30% lower than projected in the 2010 IRP.

The draft IRP update intends to decommission 12GW of old Eskom coal plants by 2030. However, the plan does not cancel the 6GW of coal power under construction and allows for a further 1GW to be built, based on two already-announced projects.

The draft assumes that no new coal power plants will be built after 2030, “unless affordable cleaner forms of coal to power are available”. This will leave South Africa with 34GW of coal capacity in 2030 – 44% of installed power capacity – down from 39GW in 2018, the plan says. (The government figure of 39GW in 2018 is lower than the Global Coal Plant Tracker’s 42GW. This lower number appears to be net of onsite consumption).

{kind=link}

{kind=link}

Coal cranes at Lethabo Power Station, South Africa. Credit: Minden Pictures / Alamy Stock Photo.

By 2050, 34GW of coal could have closed down, the plan indicates, some 83% of current current capacity. This would leave South Africa with around 12GW of coal power in 2050, less than a third of its 2018 level.

The issue of a just transition away from coal is also politically salient in South Africa and is mentioned in its NDC. Some have cautioned against the expansion of renewables due to its impact on coal-sector jobs. Employment in coal mining peaked at around 135,000 in 1981 and had fallen to 80,000 by 2015, equivalent to 0.5% of total employment in South Africa. The 2018 IRC says the government will produce a socio-economic impact analysis on the community impacts of post-2030 coal decommissioning.

South Africa is the world’s fifth largest exporter of coal, sending around 30% of its production overseas. Around half of this now goes to India, while exports to Europe are significant, but falling. Coal is an important foreign exchange earner for South Africa, accounting for around 12% of its exports. Loss of these revenues has been invoked as a risk of moving away from coal.

§ Renewables

Renewable power has risen rapidly in South Africa since 2013 and provided 3.4% of electricity in 2017, according to BP.

The cost of renewables, notably solar and wind, has fallen significantly in South Africa. Solar PV and wind costs have fallen 80% and 60%, respectively, in just four years, according to the NPC paper. New renewable capacity is now “considerably cheaper” than coal plants proposed or under construction, the ERC report says.

South Africa’s investment so far in 2018 has been the highest for five years, according to Bloomberg New Energy Finance (BNEF). Investment sat at $2.6bn in the third quarter of 2018, it says. This is a 90-fold increase compared to the same period in 2017, in part due to a $1.4bn wind project reaching financial close in August.

In 2012, South Africa replaced its feed-in-tariff scheme with a new Renewable Energy Independent Power Producer Procurement Programme (REIPPPP). This uses a bidding system to fund renewable capacity procurement, guaranteeing projects access to the grid.

The 2010 IRP included plans for 17.8GW of new renewables capacity (excluding hydro) to be installed by 2030, made up of 8.4GW of each of wind and solar PV, plus 1.2GW of concentrated solar power (CSP). This means renewables capacity in 2030 would be 18.8GW, 21% of all capacity.

The draft 2018 IRP adjusts these 2030 plans to 8.0GW solar, 11.4GW wind, and 0.6GW CSP, totalling 20GW of renewables excluding hydro. Since it also substantially reduces total capacity from all sources, this means renewables would provide 27% of installed capacity in 2030.

{kind=link}

{kind=link}

Jinko Solar photovoltaic systems by Scatec Solar, Karoo semi-desert near Hanover, Northern Cape, South Africa. Credit: imageBROKER / Alamy Stock Photo.

By the end of 2017, 8.1GW of contracts had been given to renewable energy bidders, with 3.8GW connected to the grid, according to analysis by the Council for Scientific and Industrial Research (CSIR).

In April 2018, Eskom signed off 27 agreements worth 56bn rand ($4.7bn) for a further 2.3GW of new renewable energy projects. The deal had been stalled for almost two years under Zuma. Even the signing was delayed for a month when two unions launched a legal challenge to prevent the deals from closing, citing concerns over coal jobs.

Opponents of renewable contracts have also argued that Eskom cannot afford the financial burden, even though the contracts are paid for by electricity consumers rather than Eskom itself. Doubts over Eskom’s solvency mean uncertainty and delays for new renewables are likely to continue, according to CAT.

In June, the government announced it would launch a new 1.8GW bidding round for renewables in November 2018.

The 2010 IRP and previous unpassed draft IRPs were criticised for imposing “artificial limits” on the amount of new renewables which could be built each year, even in cases where they were the cheapest option. The new 2018 draft also sets out yearly limits for renewables, arguing this “provides for smooth roll out of renewable energy” and will not impact the total amount of renewables deployed.

Hydroelectricity plays a relatively small role in South Africa’s electricity system, with only 0.7GW of installed capacity. However, it also imports 1.5GW from Cahora Bassa hydroelectric dam in Mozambique. The 2018 draft IRP includes plans for an additional 2.5GW of hydropower by 2030, which will be imported from the Democratic Republic of the Congo, meaning hydro will provide around 6% of total capacity in 2030.

§ Mining and industry

South Africa has the world’s fifth largest mining sector, which contributed 8% of its GDP in 2017. Its economy also relies significantly on heavy industry, which in turn relies largely on electricity – and, thus, coal – as an energy source. Emissions also come from industrial-process emissions, especially steel and cement production.

Policy and planning documents generally address sustainable industrial economic development, but “barely mention mitigation targets for the industry sector or concrete measures for implementation”, according to CAT.

{kind=link}

{kind=link}

Koeberg nuclear power station, Cape Town, South Africa. Credit: Johann Van Tonder / Alamy Stock Photo

South Africa has one of the most energy-intensive economies in the world, with energy consumption per unit of GDP more than twice as high as the global average in 2012. The South African government released its first National Energy Efficiency Strategy (NEES) in 2005, which aimed to reduce energy intensity of the economy by 12% in 10 years. It is now considering a post-2015 replacement, released as a draft in late 2016. This outlines plans to make energy efficiency the “first fuel” in driving sustainable economic growth in the country. It targets a 29% reduction in the energy intensity of the economy by 2030 compared to 2015, with individual targets for each sector.

However, CAT warns its proposed measures, such as the Industrial Energy Efficiency Project (IEE), may only lead to small emissions reductions. It adds:

“There are no signs of policy-driven emissions reductions in the near future for emissions-intensive subsectors [such] as steel production and mining in [the] context of the ongoing economic stagnation in South Africa.”

Uranium also plays a significant role in the domestic mining industry. However, South Africa has only one nuclear power station, the 1.9GW Koeberg plant, which is owned and operated by Eskom and has been running since 1984. It supplied 6% of the country’s electricity in 2015.

Unlike previous drafts, the 2018 electricity plan does not outline any new nuclear capacity up to 2030, although it does not exclude it from future planning. The Koeberg plant will reach the end of its life in the mid 2040s.

§ Oil and gas

South Africa has no crude oil reserves and imports 80% of its fuel. It also uses coal-to-liquid (CTL) and gas-to-liquid (GTL) technologies to produce significant amounts of synthetic fuel for the transport sector.

These expensive and energy-intensive processes are a legacy of the apartheid era, when sanctions prevented fuel imports. Last year, Johannesburg-based firm Sasol – which owns the world’s largest CTL plant – said it was turning away from the process due to low financial returns and high CO2 emissions.

Transport accounted for around 11% of South Africa’s GHG emissions in 2015, up from 9% a decade earlier. Several attempts have been made to introduce policies to reduce transport emissions, including a 2017 draft Green Transport Strategy up to 2050. While this warns the country’s transport emissions are set to roughly triple by 2050, it does not set any reduction targets.

The 2007 Biofuels Industrial Strategy, meanwhile, mandated the blending of biofuels into diesel and petrol, in theory applied from 2015. However, it has not yet been enforced, largely due to concerns over the impact of large-scale biofuels production on food security, according to CAT. The government now hopes to finalise a new biofuels regulatory framework by March 2019.

An electric vehicle (EV) roadmap was also released in 2013, but so far there are fewer than 500 EVs on the country’s roads. Efforts to introduce Bus Rapid Transit Systems to boost affordable public transport have also seen mixed success.

Gas currently plays a small role in South Africa’s energy mix, providing just 3% of total supplies in 2016. There is a small amount of domestic offshore production, with most gas imported via a pipeline from Mozambique. The 2018 IRP draft foresees an increasing share of gas power generation to complement renewables, as South Africa’s coal fleet is slowly decommissioned.

{kind=link}

{kind=link}

Dustbin art in the South African Karoo town of Prince Albert. Credit: jackie ellis / Alamy Stock Photo

In 2017, the government gave its support to shale gas exploration and extraction in the semi-arid Karoo region, citing efforts to reduce the country’s carbon footprint. In September 2018, energy minister Radebe called for all impediments to shale gas exploration to be removed as part of the government’s response to record-high fuel prices.

Analysis last year by geologists put the estimated shale-gas resource at 13tn cubic feet (tcf), equal to around 80 years worth of South Africa’s current gas consumption and around a tenth of global annual consumption. This would put South Africa 34th out of 46 nations in US Energy and Information Administration (EIA) estimates of shale resource – some 30 times less than previous estimates. It also remains unclear whether any shale resource would be economically and technically viable.

Opponents of shale gas development in the region say it will threaten its famed rugged scenery and rare wildlife, such as the mountain zebra, as well as water resources.

§ Climate laws

In 2011, the South African government approved its National Climate Change Response white paper (pdf), which aims to “effectively manage inevitable climate change impacts” and “make a fair contribution to the global effort to stabilise GHG concentrations in the atmosphere”.

However, factors such as lack of institutional capacity have restricted implementation of the white paper. A government Socio-Economic Impact Assessment System (pdf) report, published in 2017, found that the lack of legally enforceable regulations represented “a fatal risk” to achieving the aims of the white paper.

In June 2018, South Africa published a draft of a new National Climate Change Bill. Its purpose is to “build an effective climate change response and ensure the long-term, just transition to a climate resilient and lower carbon economy and society”.

The bill acknowledges that human-caused climate change “represents an urgent threat to human societies” and sets out targets for reducing emissions and the need to adapt to climate impacts.

It mandates that the government must, within two years of the bill becoming law, “establish a national environmentally sustainable development framework” to achieve the act’s objectives. It also requires the establishment of a ministerial committee on climate change with responsibility “for the coordination of climate change responses”, and a committee on climate change for each province.

{kind=link}

{kind=link}

Kinros power station near Bethal South Africa. Credit: Images of Africa Photobank / Alamy Stock Photo

Each provincial committee will be required “to undertake a climate change needs and response assessment” within the first year of the bill, and review it every five years. A “climate change response implementation plan” must then be completed within the following year.

The bill also sets out a requirement for emissions targets for “greenhouse gas emitting sectors and sub-sectors” every five years. The bill itself does not specify the ambition of these targets.

The draft bill has received a mixed response, being praised for providing “a clear signal that climate change is a cross-sectoral, holistic challenge”, but criticised for not including a specific reference to the Paris Agreement’s 1.5C warming ambition. Campaigners have also argued that the government’s pro-coal policies contradict the goals of the climate bill. The consultation period for the bill ended in August.

South Africa has also proposed legislation (pdf) for a carbon tax, which was originally mooted in a National Treasury discussion paper in 2010. The treasury published a second draft in December 2017, for consultation until March 2018. In a budget speech (pdf) in February 2018, the then finance minister, Malusi Gigaba (the position has since changed hands twice), announced that the government proposes to implement the tax from 1 January 2019. However, the new finance minister, Tito Mboweni, has since postponed implementation (pdf) – by six months to 1 June 2019 – after hearing “concerns of business and labour during the parliamentary hearings”.

The tax would cover emissions from fossil fuel combustion, industrial processes, product use emissions, and fugitive emissions from mining. It would potentially increase petrol and diesel prices by up to 23 and 29 cents per litre (approximately 1-2%), respectively. The tax has been criticised by the steel and mining industries as unaffordable.

The tax would be set at 120 rand (around $8) per tonne of CO2 equivalent. However, during the first phase up to 2022, a basic tax-free threshold of 60% of emissions, plus additional allowances, may mean around 95% of emissions are exempt. This would put the effective tax rate at around R6-48 ($0.4-3) per tonne.

(Update 29/3/2019: In February 2019, South Africa’s parliament approved the long-delayed carbon tax bill. The new law allows a tax rate of 120 rand ($8.48) per tonne of CO2 equivalent. It also confirms that total tax-free allowances can be as high as 95% during the first phase.)

New passenger vehicles are also subject to a carbon emissions tax, which was effective from 1 September 2010. It has a flat rate of R75 (around $7) for each gram per kilometre above 120g/km, incorporated into the price of new cars.

§ Impacts and adaptation

Average temperatures in South Africa have risen around one and a half times as quickly over the past five decades as the global average of 0.65C. Maximum and minimum daily temperatures have been increasing in almost all seasons and regions. (Search for places within South Africa in Carbon Brief’s global map of rising local temperatures.)

Changes in rainfall show weaker trends, but there is a tendency towards a decline in the number of rain days in almost all regions. In contrast, extreme rainfall events have increased in frequency, particularly in spring and summer.

The impact of climate change has been brought to the fore with the recent severe drought in the Cape Town region and the lingering threat of “Day Zero”, when taps in the city run dry and residents would be required to queue for water.

{kind=link}

{kind=link}

A rapid assessment attribution study found that human-caused climate change made the lack of rainfall that led to the three-year drought around three times more likely.

Agriculture in South Africa faces a variety of risks associated with climate change, such as changing rain patterns, increased evaporation rates, higher temperatures, increased pests and diseases, shifting growing regions and reduced yields.

On 31 August 2018, South Africa submitted its third National Communication report under the UNFCCC. The report highlights trends and projected changes in climate and provides an inventory on GHG emissions.

Projections for the future suggest that under an intermediate emissions scenario (RCP4.5), South Africa is likely to warm by 2-3C by mid-century, reaching 3-4C and beyond by the end of the century. Under a no mitigation, business-as-usual emissions scenario (RCP8.5), warming could exceed 4C across the whole country by the end of the century, even surpassing 6C in some western inland areas.

Rainfall projections are generally less clear-cut, but predominantly suggest a significant decrease in average rainfall towards the middle and end of the century.

According to its National Communications report, South Africa has a rich biodiversity containing almost 10% of the world’s total known bird, fish and plant species, as well as around 6% of mammal and reptile species. The habitats of these species are projected to change dramatically in a warmer, drier climate.

The South African government is currently developing a National Climate Change Adaptation Strategy, which will serve as its submission of a National Adaptation Plan to the UNFCCC. A second draft (pdf) of the strategy was issued for consultation in October 2017. A final draft is expected this year.

Its “strategic outcomes” include producing adaptation plans that cover at least 80% of the economy by 2025; implementing an adaptation, vulnerability and resilience framework across all “key adaptation sectors” by 2020; and defining and legislating for adaptation governance through the new National Climate Change Bill.