Analysis: How BP’s energy outlook has changed after the Paris agreement

A year has passed since the last BP energy outlook. In that time, 195 countries have sealed a global climate change agreement in Paris which promises to achieve net zero emissions this century.

Yet the 2016 BP energy outlook, published this week, shows the oil company’s views on the shape and direction of energy demand over the next 20 years have barely shifted.

Carbon Brief explores why BP’s outlook appears impervious to the world’s first universal, global commitment to cut emissions.

§ Models are wrong

Before looking at the findings of BP’s outlook, it’s worth remembering that it is a modelling exercise. While models can be useful, they’re always wrong, particularly when it comes to energy.

Forecasts often say more about the assumptions of the modellers than anything else. The most rigorous projections explore a range of plausible assumptions.

Aware of these limitations, BP’s outlook starts with a hefty disclaimer that’s worth quoting from:

Forward-looking statements involve risks and uncertainties because they relate to events, and depend on circumstances, that will or may occur in the future. Actual outcomes may differ depending on a variety of factors.

§ Likely outlook

Now that we’ve got the small print out of the way, let’s turn to the main findings of the outlook. The report’s focus is a “base case”. This is the “most likely” future scenario, according to BP.

Has that future shifted as a result of the Paris climate agreement? Has its expectations shifted after 189 countries pledged to tackle their emissions?

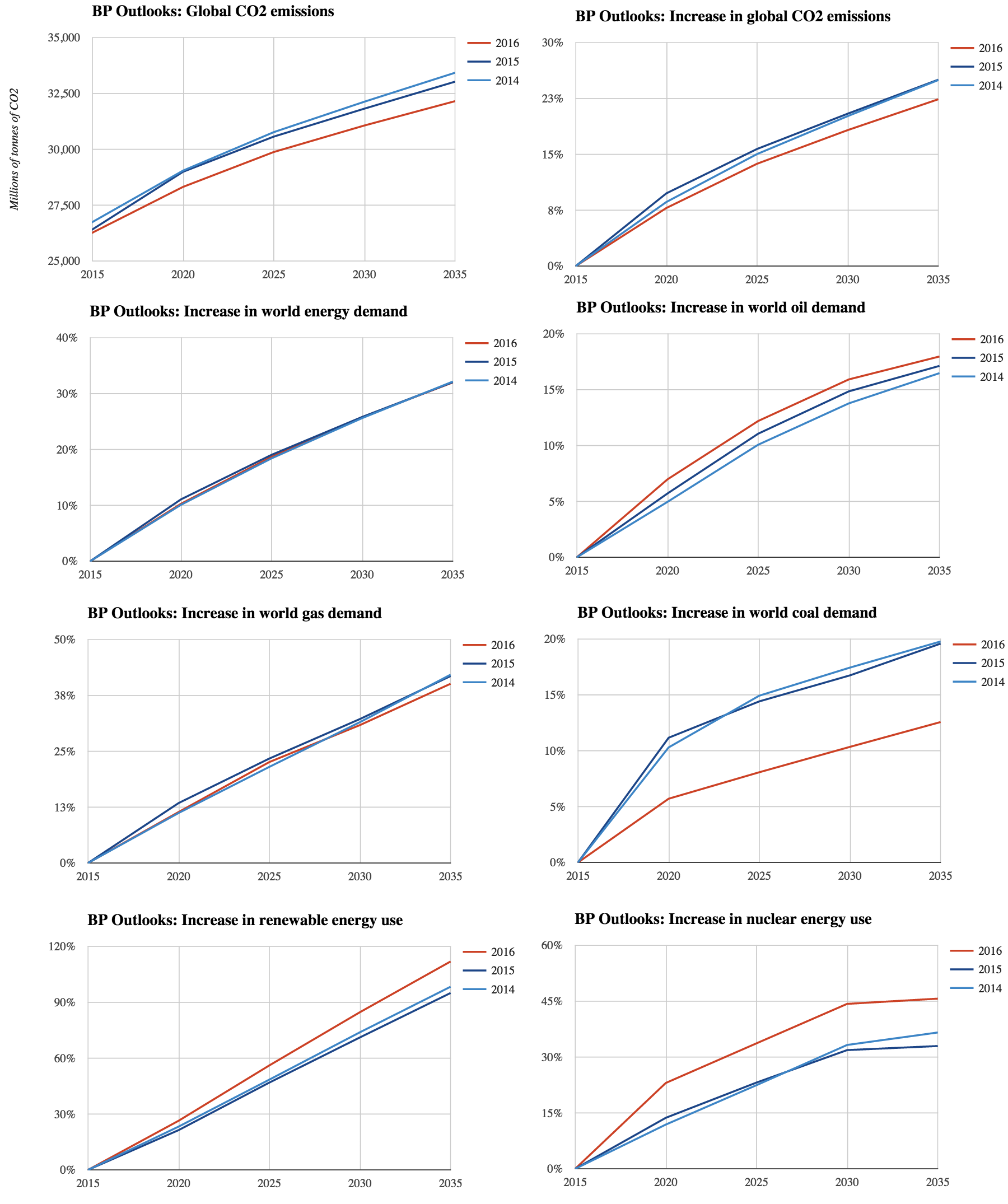

The charts below compare the path of energy and CO2 emissions growth between 2015 and 2035, according to BP’s energy outlooks from 2014, 2015 and 2016.

The most striking feature is how little has changed. It is almost as if Paris never happened. Where there are differences, economic factors seem to be at work rather than the climate treaty.

{kind=link}

{kind=link}

Forecasts from 2014 (light blue), 2015 (dark blue) and 2016 (red). Top left: global CO2 emissions from fossil fuel use (millions of tonnes). Other charts: % change in energy demand or emissions, against a 2015 baseline. Source: BP energy outlooks. Charts by Carbon Brief.

The latest outlook has CO2 emissions from fossil fuel use reaching 32.2bn tonnes in 2035, less than 3% lower than BP’s pre-Paris expectation of 33GtCO2. It now thinks emissions will rise by 23% between 2015 and 2035, rather than the 25% increase it expected a year ago.

Similarly, BP’s outlooks for overall energy use, as well as oil and gas demand, seem unaffected by Paris. Its forecast for oil has actually increased over the past year, because oil prices have fallen.

Increasing energy demand is a central tenet of oil company forecasts. As populations increase and incomes rise, they argue, demand for energy will continue to rise.

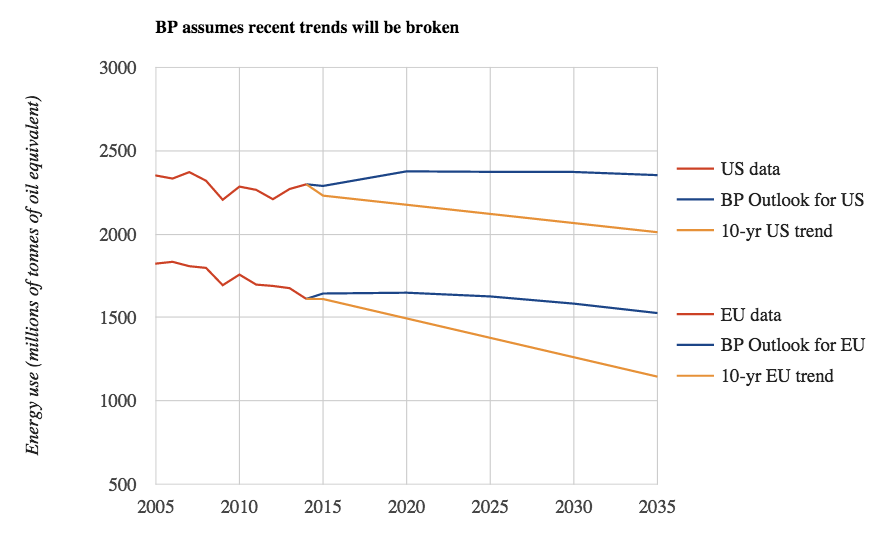

BP’s outlooks for the US and EU illustrate the consequences of these assumptions. Whereas US and EU energy demand has been falling relatively consistently over the past decade, BP expects this trend to be reversed (chart, below).

Not only is BP’s forecast inconsistent with recent trends, it also implies that the EU will miss its own energy efficiency targets for 2020 and 2030. The EU is currently roughly on-track to deliver its 2020 target and will present legislation towards the 2030 goal later this year.

{kind=link}

{kind=link}

Total primary energy demand in the EU and US between 2005 and 2014 (red). Forecasts from the 2016 BP energy outlook (blue) are shown with a continuation of the trend over the past 10 years (yellow). Source: BP Statistical Review of World Energy 2015; BP Energy Outlook 2016. Chart by Carbon Brief.

BP considers alternative scenarios for energy demand, including the consequences of slower economic growth or faster uptake of low-carbon and energy efficiency. Global demand for oil and gas would still increase, BP says, albeit more slowly.

Some analysts think the oil industry systematically over-estimates its own growth prospects by underplaying the importance of fuel efficiency standards, subsidy reforms and alternative fuels. For instance, BP’s outlook sees electric vehicles claiming a tiny share of future transport demand.

Speaking at a Chatham House event earlier this month, Prof Paul Stevens, Chatham House fellow on energy, environment and resources, said much of the expected increases in oil demand projections comes from India, China and the Middle East.

These countries have been busily reforming fuel subsidies, he noted, suggesting demand may be weaker than expected. For China, Stevens said projections tended to be “horribly overstated”. The BP Outlook sees China’s oil demand rise by 63% by 2035.

§ Renewables up, coal down

As we’ve seen, BP’s outlook is in many ways unmoved by Paris. However, there are some large adjustments in the latest edition for coal and renewables, hinting at brighter news for the climate.

As BP notes, it has consistently had to raise its expectations for renewables in successive outlooks since 2010. It is not alone in having underestimated the growth of clean energy. This year’s upwards revision is the biggest ever, yet the outlook still looks to be behind the curve.

BP says: “Renewables are expected to account for more than a third of EU power generation by 2035”. This sits awkwardly against the fact that renewables already supplied a third of EU power in 2014 and continue to expand rapidly.

The 2016 outlook also includes a sharp downwards revision to coal forecasts for 2035, as the chart above shows. BP attributes this largely to reform of China’s economy, rather than Paris.

Like BP, the International Energy Agency (IEA) recently trimmed its outlook for coal. Nevertheless, both insist the fuel will see a return to growth, after falls in global demand in 2014 and 2015.

Could coal use fall rather than rise? The IEA says China might have peaked in 2013, which would mean falls in global demand, while BP considers a “faster transition” scenario where coal use falls out to 2035 as a result of more rapid uptake of renewables and efficiency.

§ Paris goals

BP’s forecasts make grim reading for those interested in avoiding dangerous climate change. Its most optimistic “faster transition” scenario sees emissions starting to fall in the late 2020s, yet the reductions remain far short of what would be needed to limit warming to 2C — let alone 1.5C.

The shift towards low-carbon fuels and increases in energy efficiency are “unlikely to deliver the sharp fall in carbon emissions called for in Paris”, writes Spencer Dale, BP group chief economist, in an opinion piece for the Financial Times.

Luke Sussams, a senior analyst at the Carbon Tracker Initiative, says in a statement:

BP’s energy outlook to 2035 has changed little over the last year. It appears to state the COP21 international climate change agreement will make little impact in suppressing future fossil fuel demand.

Peeling back the layers of BP’s outlook exposes how its modelling appears to struggle to replicate current trends in efficiency and low-carbon. Yet it’s important to remember that BP’s efforts are inherently limited, as are other similar efforts. That’s why BP’s outlook starts with a disclaimer.

For instance, no model could have predicted that Vietnam would announce a shift away from coal post-Paris, having previously been seen as one of the world’s biggest growth markets. The future of coal in India is also tough to forecast. Along with big plans to build out coal power, it faces a growing air pollution crisis that could, like in China, force the government to change course.

Models will always struggle to capture the fast-changing, unpredictable nature of global economic and political change. The Paris climate deal is a case in point. Its success or failure will not be decided by models. Instead, it must rely on the world’s ability to confound modellers’ predictions.