Does the financial sector believe in unburnable carbon?

High carbon assets, like coal plants, may dramatically lose value as a result of policies aimed at reducing greenhouse gas emissions, according to a report launched last year. A research programme to be launched by the University of Oxford on Monday aims to help the business community and policymakers take the risks into account. But how will investors and the regulators respond?

Stranded assets?

Oxford’s new programme builds on the work of the Carbon Tracker initiative, which launched its report, ‘ Unburnable Carbon‘, last year.

The world’s financial markets are out of sync with climate policies, the report says. Markets “have an unlimited capacity to treat fossil fuel reserves as assets”, it says, but if policies are brought in to limit temperature rise to two degrees above pre-industrial levels, most of the earth’s fossil fuel reserves will have to stay in the ground. That means they’ll be off limits as assets.

The report draws on work by the Potsdam Institute, which calculated what it calls a global carbon budget for 2000-2050. Its calculations set a limit on carbon emissions that would reduce the risk of the temperature rising more than two degrees above pre-industrial levels to twenty per cent.

Carbon tracker concludes that if the world keeps within its carbon budget, up to 80 per cent of reserves held by the world’s largest coal, oil and gas companies would be essentially useless – or in more technical terms they would be ‘stranded assets’.

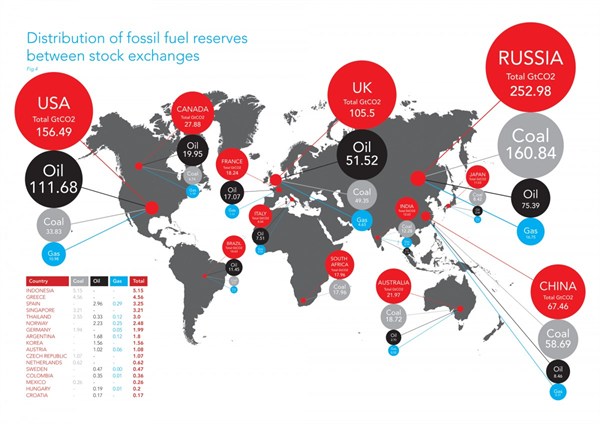

Image - carbontracker_map (note)

{kind=link}

{kind=link}

The world’s fossil fuel reserves. But how much of it is ok to use?

The report says says treating high carbon assets as though there’s no limit to exploiting them poses systemic risks to capital markets and, ultimately, everyone’s economic prosperity.

Who cares?

This raises an interesting question: is the financial community likely to take any notice? About a year ago, several big cheeses including the chief executive of Aviva Investors, Zac Goldsmith MP and Lord Deben sent an open letter to the head of the Bank of England, Mervyn King, raising the problem of stranded high-carbon assets.

To the layperson, King’s response sounds pretty equivocal. He argued that three conditions would need to be fulfilled before he accepted the argument.

First, that the market’s exposure to carbon-intensive investments would need to be significant enough to pose a problem. Second, King needs to be sure that the risks are not already accounted for by the market – for example through the carbon price. Thirdly, the policy changes would have to take place “in an insufficiently long period of time for the relevant financial institutions to adjust their portfolios in an orderly manner”.

King’s letter concludes:

“The necessity of all three conditions being met raises a question in our minds as to whether or not this is a potential threat to financial stability â?¦ Nevertheless â?¦ we we will endeavour to to include this in the list of topics we regularly discuss with market participants, to assess whether or not this is a risk of which they are aware and the extent to which they are taking it into account in their investment decisions”.

Ben Caldecott, head of policy at of Climate Change Capital and one of the initiators of the letter argued that it was ‘important’ and ‘encouraging’ that the governor had accepted the need to consider the problem at all.

Oxford pressure

Caldecott explained to us that financial institutions are “only just starting to understand” the problem of stranded high carbon assets. He heads up Oxford’s new programme, which he says is designed to produce “rigorous and robust work” that will convince financial institutions that they’re taking a significant risk by failing to take account of stranded assets.

The research programme aims to create new tools to help manage the risks and respond to them – for example by helping businesses develop different scenarios for the future or systems for weighing up future risks, or by developing more sophisticated risk management systems.

And while the head of the bank of England may not be convinced of the risk yet, some businesses are already starting to sit up and take notice. Late last month for example market analysts at bank HSBC released a report warning that major oil and gas companies – including BP, Shell and Statoil – could face a loss in market value of up to sixty per cent if the international community sticks to its promises to reduce emissions.

Some way to go

The dichotomy between the way the financial markets are structured and the imperative to reduce emissions has attracted some attention over recent months. Economist Nicholas Stern for example commented on the ” fundamental contradiction” between the way fossil fuel reserves are assessed and global climate policy.

But will such wider considerations filter through to the rough and tumble of the markets? A couple of weeks ago Jo Confino of the Guardian wrote a somewhat despairing piece about the chances that actuaries – tasked with assessing the future risks affecting pension funds – will be able to take the issues on.

In the end, the hypothesis that high-carbon assets will be affected by climate policies is also predicated on the assumption that the policies themselves will be implemented.

If they are not, then the financial community may be more justified in failing to respond – but the world could face a different, and even more challenging, set of risks from a changing climate.