The IEA’s coal projections on demand and emissions

A report released earlier this week from the International Energy Agency (IEA) predicts global coal demand will grow by 16.9 per cent over the next five years, or 2.6 per cent per year. This is largely thanks to to the pace of growth in China – the report says that if economic growth in China continues on its current pathway, it will consume more coal than the rest of the world combined by 2014. This far outweighs a predicted reduction in coal demand in the US, where the IEA says cheaper natural gas has encouraged a switch away from coal.

We take a closer look at the IEA’s report to find out what’s happening to coal consumption in wealthy and developing countries, and ask how changing demand will affect greenhouse gas emissions.

Coal demand falters in developed countries

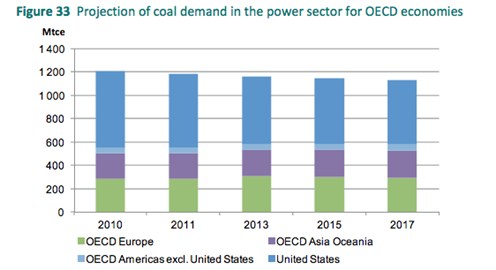

The IEA predicts that across a group of the world’s richest nations – members of the Organisation for Economic Co-operation and Development (OECD) – the amount of coal used to generate electricity will fall by 0.8 per cent per year over the next five years.

But despite this fall and the growth of gas and renewables, coal will remain the main fuel for generating electricity in OECD countries.

According to the report, the use of coal to generate power will increase 1.3 per cent each year in developed countries in Asia and Australasia. Coal demand is expected to rise in some European countries, but the IEA predicts that public opposition to coal and the closure of many old coal-fired power plants is likely to limit growth. This means that across the European OECD region as a whole, coal demand will likely change little. The IEA also predicts the carbon price set by the European Emissions Trading Scheme will go up in the future, which makes burning carbon-intense coal less economic.

The biggest change to coal demand in richer countries comes from the United States, where the IEA predicts an increase in cheap gas will push out coal use in the power sector, with consumption predicted to fall 2.4 per cent each year.

Image - Fig 33. Power Coal (note)

{kind=link}

{kind=link}

Coal used outside of power generation, for example in industry and for heating, is also projected to fall 0.5% each year in the OECD region. These non-power uses account for around a fifth of total coal use.

Coal demand booms in developing countries

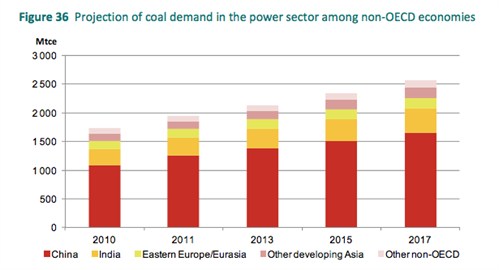

Coal use in countries that are not part of the OECD will rise, the IEA says. Led by continuing economic growth in China and India, coal demand for electricity generation is projected to increase 4.7 per cent each year.

Assuming its economy continues to grow at a fast pace, China will see the largest increase in coal use in the power sector in absolute terms. But in percentage terms, other non-OECD countries in Asia like Indonesia and Vietnam will see bigger increases in demand for coal.

In Eastern Europe, natural gas will still play a central role in power generation, so the increase in coal demand is expected to be slower than elsewhere – around 2.3 per cent each year.

Image - Fig 36. Power Coal (non) (note)

{kind=link}

{kind=link}

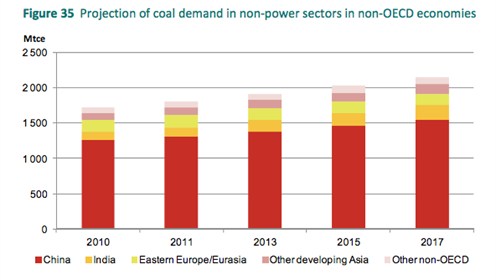

In poorer countries, a significant proportion of coal use is for heavy industry and heating purposes, rather than generating power. IEA figures show that in 2017, these non-power uses will account for 46 per cent of demand, while power generation will account for 54 per cent of demand in non-OECD countries.

That makes a three per cent growth in non-power coal demand each year quite significant. The majority of this growth is, again, expected to come from China, where coal is used heavily in industry and for fuel in homes. In relative terms, India will see the fastest growth in coal demand.

Image - Fig . 35 Non Power Coal (non) (note)

{kind=link}

{kind=link}

Consequences for greenhouse gas emissions

As global demand for coal increases, greenhouse gas emissions are also set to rise – especially with technology to capture carbon emissions still in its infancy.

The IEA predicts that in OECD countries the decline in coal burning over the next five years will reduce carbon dioxide emissions by 250 million tonnes. But that will be far outweighed by an increase of about 3500 million tonnes of carbon dioxide, as coal consumption intensifies in the non-OECD world.

The report calculates that by 2017, a quarter of coal-based carbon dioxide emissions will come from OECD countries, and three quarters will come from non-OECD countries. It’s worth pointing out though that many coal-intensive industries like steel and cement production are based in developing countries, producing goods that developed countries then import. That means a chunk of those emissions are shifted from OECD countries to non-OECD countries.

Conclusion

The growth in coal demand doesn’t look like good news for plans to reduce greenhouse gas emissions. Coal-related emissions could be somewhat constrained if China’s economic growth slows sooner rather than later, but with many other countries also relying on coal to expand heavy industries, heat homes and generate increasingly more electricity, greenhouse gas emissions are likely to keep rising.