Shale gas could restrain rising energy costs, says report

A thriving European shale gas industry could help limit energy bills rises by the middle of the century, according to a new report from two respected energy consultancies. The report – which is sponsored by the oil and gas industry – also predicts that shale gas won’t threaten Europe’s plans to reduce carbon emissions.

In a time of rising energy bills, the question of whether shale gas could provide the UK with a source of cheap gas has attracted a considerable amount of media attention. The consensus of expert opinion suggests that indigenously produced shale gas is unlikely to have a significant impact on gas prices in the UK – at least in the short-term.

Yesterday’s report projects the impacts of developing a shale gas industry across the whole of the EU, over several decades. It predicts household spend on gas and electricity could be cut by 11 per cent in relative terms as a result of European shale gas – although that doesn’t necessarily mean that bills will go down in absolute terms.

The International Association of Oil and Gas Producers (OGP) commissioned the report, which might invite scepticism about its relatively optimistic conclusions. But the two consultancies who created the analysis – Poyry consulting and Cambridge Econometrics – emphasise that it was conducted independently, without involvement of the OGP members.

What are the assumptions?

The study analyses three different scenarios for what the European shale gas industry might look like over the next four decades.

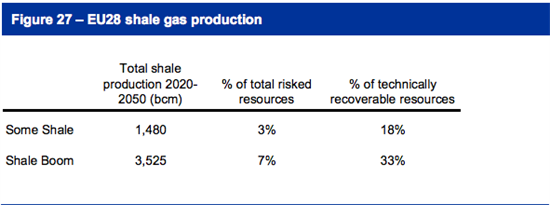

In the ‘no shale’ scenario, shale gas isn’t developed at all. The central scenario – ‘some shale’ – assumes that a shale gas industry goes ahead, but environmental, technical or economic limitations prevent it reaching its full potential. In this scenario, 15 per cent of shale gas in the ground is ‘technically recoverable’, but only three per cent is ultimately extracted.

Image - Screen Shot 2013-11-26 At 13.56.46 (note)

{kind=link}

{kind=link}

Source: Macroeconomic effects of European shale gas production, November 2013. Under the ‘some shale’ scenario, 15 per cent of total shale gas in the ground is technically recoverable. 18 per cent of that is ultimately recovered – or three per cent of the total.

The ‘boom’ scenario is more optimistic, predicting the development of a large European shale industry. Under this projection, 20 per cent of the shale resource is technically recoverable, and a third of that – seven per cent of the total – is ultimately extracted.

To provide some comparison, the British Geological Society says that in the US it has been possible to extract ten per cent of the total amount of shale gas in the ground.

Poyry consulting’s lead author John Williams tells Carbon Brief that he views the ‘shale boom’ scenario as “achievable” but optimistic, while ‘some shale’ takes a “more conservative” view of shale gas development.

Cutting bills – relative to what they would have been

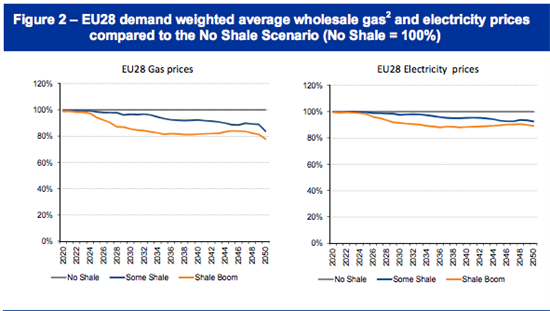

A European shale gas industry could cut the costs of electricity and gas, the report finds.

Under the some shale scenario, wholesale gas prices are on average six per cent lower than they would have been otherwise, across the whole period studied. Under the boom scenario, wholesale gas prices are 14 per cent lower on average – and by 2050 consumer energy bills are up to 11 per cent lower than they would otherwise have been.

Image - Screen Shot 2013-11-26 At 11.53.35 (note)

{kind=link}

{kind=link}

It’s important to note that this is not a prediction of what will actually happen to consumer energy bills over the next few decades. For the sake of the modelling, the report artificially assumes that wholesale energy prices will remain absolutely steady if shale gas isn’t developed, and so refrains from making any predictions about absolute price changes.

Author John Williams tells Carbon Brief that in his view wholesale energy prices “certainly don’t reduce from where we are today” over the next few decades. It’s more likely that European shale gas will be offsetting – or partially offsetting – further increases in gas and electricity prices.

Shale gas doesn’t increase emissions

Some experts have expressed concern that a new source of cheap gas won’t be good news for carbon emissions – because it could mean the UK burns more gas, and gets less power from renewables.

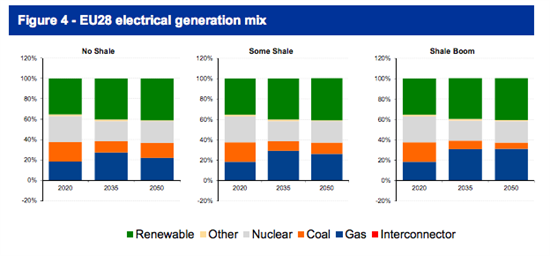

According to yesterday’s report, this isn’t going to happen. It suggests that instead of displacing renewables, European shale gas means the continent burns less coal. Natural gas releases about half the carbon emissions that coal does when burnt. So burning gas instead of coal means less emissions.

Image - Screen Shot 2013-11-26 At 11.56.08 (note)

{kind=link}

{kind=link}

Generation from coal declines under all the report’s scenarios. It also assumes that some countries – including the UK and France – fail to replace their current fleet of nuclear power stations. This leaves quite a lot of space for gas. Under the more optimistic shale gas predictions, slightly more gas is burnt, and indigenously produced gas also replaces imports.

The report doesn’t look at what happens if the EU expands the amount of power it gets from renewables at a greater rate than expected, however. It assumes the EU just misses its target to source 20 per cent of power from renewables by 2020, and it doesn’t take into account any future renewables targets. This is based on the consultancies’ current projection of what the future holds, and the normal caveats about predicting the future apply.

If the continent continues to expand renewables at a more ambitious rate than expected, then shale gas and low-carbon energy may come into conflict.

Predictions are hard, especially about the future

Shale gas hasn’t yet been developed on a commercial scale in the EU – which inevitably means that reports like this one have to make a series of assumptions about what how successful a nascent shale gas industry will end up being.

As many experts have already pointed out, there are a number of barriers to a European shale gas industry that don’t apply in the USA – including different geology, regulation and a much greater density of population. The experience of several countries to this point highlights some difficulties. France, for example, currently has a moratorium on shale gas – a fairly significant political block. In Poland, the government is enthusiastic about the new fuel, but the industry faces problems that are affecting its development.

So developing shale gas across the EU is a complicated prospect. Nonetheless, having spoken with one of the authors of the report, he is convinced that the central scenario in the report fairly reflects these limitations, and provides a conservative assessment of what might actually happen.