Government fails to bring clarity to electricity market reforms

The government yesterday outlined how it plans to deliver a low carbon economy. It was hoped the Department of Energy and Climate Change’s (DECC) much anticipated report would clarify how the government’s proposed electricity market reforms (EMR) could affect the UK’s future energy mix. But the new report looks more like the government keeping its options open than a confident stride down a path towards a decarbonised energy sector.

Three paths to decarbonisation

One of the most high profile disputes about the forthcoming energy bill centred on whether or not to include a target to limit electricity generation emissions to 50 grams of carbon dioxide per kilowatt hour by 2030. An amendment to force the Energy Secretary, Ed Davey, to set a target in the current energy bill was narrowly defeated last month. Despite this, Davey maintains the government will set a target in 2016.

While DECC’s latest report does include a scenario where that target would be met, it also models the possibility of electricity generation having a much higher emissions intensity of 200 grams per kilowatt hour – a scenario first introduced its gas strategy document last year.

Environmental campaigners have criticised DECC for continuing to include the scenario which would mean missing a legally binding emissions reduction target. But DECC’s main analysis focuses on its central scenario of limiting electricity generation emissions intensity to 100 grams per kilowatt hour – the level favoured by the Liberal Democrat ministers.

The three scenarios show what the energy mix would look like if a lot of carbon capture and storage (CCS) technology comes online, if offshore wind costs reduce dramatically, or if nuclear generation capacity doubles.

The scenarios are designed to show what could happen if a particular form of generation turns out to be much better value than others due to reduced technology costs or low fossil fuel prices. DECC is coy about which one it favours, however – with the report saying the scenarios “are indicative”, and that “the electricity generation mix through the 2020s is unlikely to match any one of these scenarios exactly”.

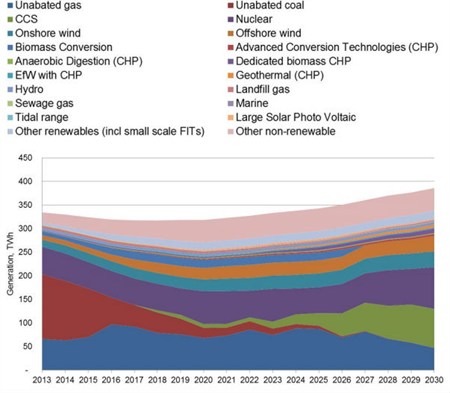

1. What if we build CCS?

Developing technology which can capture carbon dioxide emissions from power plants and lock them away is going to be essential if the UK is going to decarbonise while continuing to use fossil fuels, the government reckons.

One of DECC’s scenarios assumes three CCS plants are built by the end of 2020, with coal and gas generation ramping up throughout the 2020s to get 83 terawatt hours of electricity generated by plants with CCS fitted in 2030.

For that scenario to occur, the cost of CCS generation would need to be around £85 to £160 per megawatt hour. It would also require gas and coal prices to stay low.

But predicting fuel prices is notoriously difficult, and DECC was today accused of underestimating the impact unconventional fuels such as shale gas could have on future gas prices.

Image - DECC high CCS (note)

DECC scenario showing higher deployment rate of CCS

{kind=link}

{kind=link}

There are currently no commercial-scale CCS plants in operation in the UK, and potentially only one new European project in the pipeline – meaning the cost of installing CCS would need to fall rapidly to make this level of investment value for money.

DECC concedes that there is “considerable uncertainty at this stage of CCS development as to which technologies will prove the most cost effective in the long-term” – meaning this much CCS may be unlikely, even if gas and coal prices remain competitive with renewable energy.

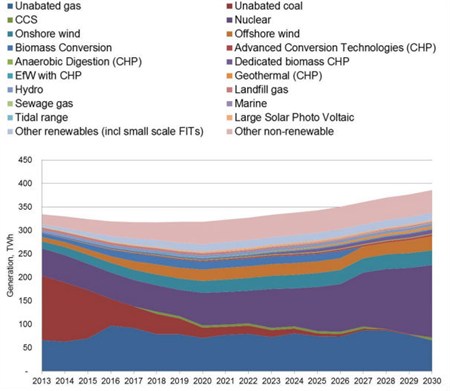

2. What if we build more nuclear?

Another of DECC’s scenarios projects 20 gigawatts of nuclear generation capacity in 2030, generating 154 terawatt hours of electricity. Nuclear contributed 69 terawatt hours of generation in 2011 from about 10 gigawatts of installed capacity.

The government is currently locked in negotiations with French energy giant EDF to build two new 1.6 gigawatt reactors at Hinkley in Somerset. Japanese technology company Hitachi are planning to build 6 gigawatts of new nuclear, and UK nuclear company NuGen have plans to build another 3.6 gigawatts in West Cumbria over the next decade – but that’s still about 4 gigawatts short of the nuclear capacity projected in DECC’s scenario.

Given the difficulties in striking a deal with EDF and cost overruns and delays in other European nuclear builds, getting 20 gigawatts of capacity online by 2020 could be a tall order.

Image - DECC high nuclear (note)

DECC scenario showing higher deployment rates of nuclear

{kind=link}

{kind=link}

The scenario assumes nuclear electricity costs around £85 per megawatt hour in the mid 2020s. But government negotiations with EDF are being held up as they try to agree on a guaranteed price for the new plant’s electricity – known as the strike price.

Strike price estimates range from £80 to £100 per megawatt hour for a contract potentially up to 40 years long. With those negotiations ongoing, the report stresses that the price assumption behind the scenario “should in no way be seen as a guide to potential strike prices for early new nuclear power plants”.

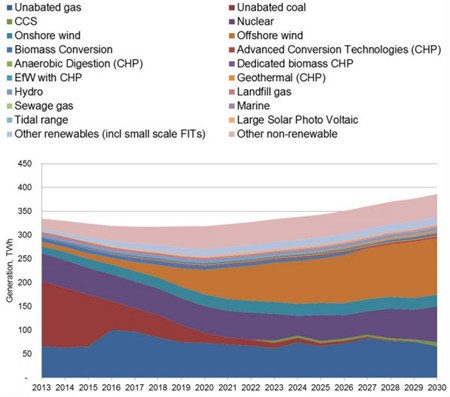

3. What if we build more offshore wind?

The final scenario projects offshore wind generating 120 terawatt hours of electricity in 2030, with 39 gigawatts of turbines installed. The UK currently has just over 3 gigawatts of operational offshore wind capacity.

Image - DECC high wind (note)

DECC scenario showing higher deployment rates of offshore wind

{kind=link}

{kind=link}

Offshore wind generators are guaranteed to receive £155 per megawatt hour from 2014, falling to £135 by 2020. But in this scenario, the cost of offshore wind electricity is £95 per megawatt hour in 2025.

The report says incentivising this much offshore wind investment would require technology costs to fall significantly while government support levels stay high. Keeping subsidies at about the same level for another decade despite falling generations costs could potentially be an expensive policy decision, though – with consumers footing the bill.

Another piece of the puzzle

Energy generators were hoping DECC’s delivery plan would bring some clarity to how the government hopes to secure investment in the UK’s energy sector while meeting its emission reduction target. The industry has broadly welcomed the report as another piece of the EMR puzzle.

But by outlining three technology scenarios DECC says could but probably won’t happen, and continuing to model a wide range of decarbonisation trajectories, the government has failed to provide the certainty industry craves. So energy providers – and consumers – are not really any wiser to the government’s plans for the energy mix than before.