How climate-ready is your house?

Are you pulling out all the stops to climate-proof your home? Have you installed ceiling fans, planted trees for shade and taken out flood insurance? It’s unlikely you have, according to a new study of household actions in the UK.

While we make simple actions to deal with a cold snap or heatwave, the research finds, households are struggling to prepare for long-term changes in climate.

What action can you take?

As global leaders prepare to convene in New York to discuss how to curb greenhouse gas emissions, a new paper discusses another side to limiting climate change – adaptation.

Adaptation means taking steps to increase our resilience against climate change that our past emissions have already committed us to, impacts that are now unavoidable.

The study, published in the journal Climatic Change, looks at adaptation measures people can take in their own homes. And the good news is, some actions are easy. You’ve probably done many without even realising. Putting on an extra jumper in a cold spell or eschewing the Sunday roast in favour of a salad during a heatwave are both adaptive responses.

Some actions aren’t as simple as changing your diet or dipping into your wardrobe, however.

The study looks reviews published research on climate adaptation in UK households and finds that while we’re pretty good at doing the easy things, we’re not so great at making plans for the long-term.

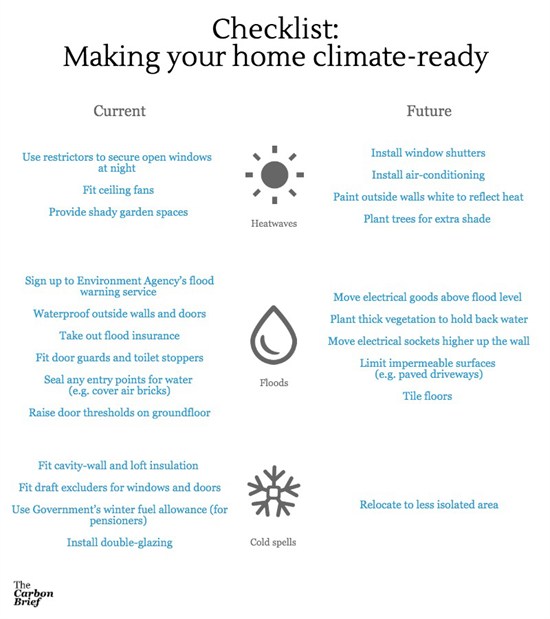

A checklist

The paper runs through some adaptation options available to UK households, which we’ve illustrated in a checklist below. The list on the left are examples of actions for managing current risks, while the list on the right shows how to climate-proof for the longer-term.

Image - Making Your House Climate Ready InfoG (note)

{kind=link}

{kind=link}

Examples of UK household adaptation actions in the short term (left-hand list) and long-term (right-hand list). Porter et al. (2014). Infographic created using Piktochart

What affects our actions?

So what makes us take measures to protect our homes? Previous experience of weather extremes is one factor, according to the research – a simple case of once bitten, twice shy.

Other reasons include the potential to make long-term gains from money invested. And how socially acceptable the action is perceived to be – you may be happy to sit in a cold house surrounded by blankets, the study argues, but it’s unlikely you’d make visitors do the same.

If we’re less likely to make adaptation plans for the long term, as the study argues, what’s stopping us?

Cost is a key reason, say the researchers. Evidence suggests that investments to minimise extreme cold or hot temperatures are closely linked to the ‘payback time’; for example, how long it would take saving on fuel bills to add up to the cost of double-glazed windows.

Other barriers the study identifies include difficulty finding the right people to do the work, and coping with the disruption. Major changes to a house will require qualified professionals and maybe even planning approval.

In the case of flooding, the reasons are different. The study finds householders act to protect their own property and preserve the value of the house. The incentive to reduce insurance premiums – or threat of losing cover – can influence householders to invest in flood protection for their home, as can ensuring that a future buyer would be granted a mortgage.

But some don’t respond at all. Many householders assume the government takes responsibility for protecting their house and so don’t see the need to take preventative action themselves, the researchers suggest.

And there is also an emotional response. As lead author Dr James Porter, tells us:

“Accepting risk changes your perception of your house as a sanctuary – your safe place. By fitting door guards or toilet stoppers, you’re acknowledging that your home is at risk from flooding and people don’t seem to want to do that.”

Do we act of our accord?

So what would encourage householders to do more to adapt their property?

The study shows households don’t need government intervention to choose the easy, low-cost adaptation actions. But financial incentives are necessary to encourage longer-term actions.

That said, the study finds available financial incentives are going unused. For example, less than a third of government grants to help with insulation and flood-proofing have been taken up, suggesting the public is either unaware of them or disinclined to take advantage.

What might help people access these incentives? Porter suggests awarding grants on an individual basis perhaps isn’t the best approach:

“The people who get the grants are the ones who are aware of them. Neighbourhood or community-scale grants might be a better way to go – if you see your neighbours making changes then you might follow.”

So householders are unlikely to take action towards making their homes climate-ready without a fair bit of help, the study concludes. The implication is that new initiatives from government or the private sector would be needed to encourage long-term adaptation.