How the global market is pushing up UK gas prices

UK energy bills are set to go up by 2020 as the country becomes more dependent on imported gas, says energy regulator Ofgem. So how are international gas markets shaping up in future, and how will they affect what we pay for gas in the UK?

Since 2004, the UK has been a net importer of natural gas, meaning the country’s domestic supplies can no longer meet demand. Head of Ofgem Alastair Buchanan wrote in the Telegraph today that the amount of of UK power generation from gas may have to go up around 30 per cent by 2020 to fill the gap left as the country decommissions old coal power stations. And increasing exposure to global gas markets means the price we pay for energy is likely to go up.

The UK and international gas markets

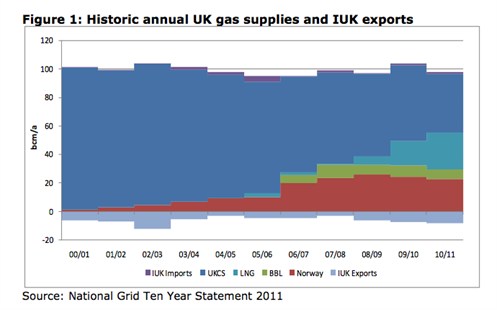

Over the last decade, the amount of gas the UK imports from other countries has steadily increased. According to an Ofgem report last November, the country now gets much of its gas from Norway, Europe, Russia, and liquid natural gas (LNG) imports from places like Qatar, the world’s biggest exporter.

Image - Screen Shot 2013-02-19 At 11.11.01 (note)

{kind=link}

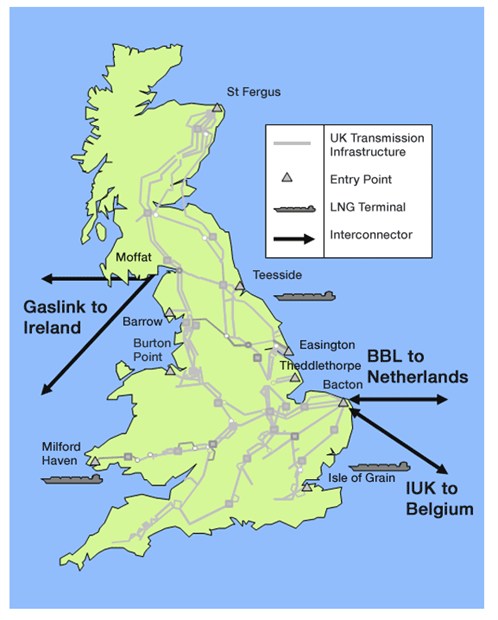

Norwegian and Russian gas comes to the UK by pipeline. LNG, meanwhile, is compressed and transported to the UK by tanker. Both types of gas are used in the same way – piped into homes, or used to power electricity plant, for example.

Image - Screen Shot 2013-02-19 At 14.09.44 (note)

{kind=link}

Source: National Grid

According to a 2012 report by BP, LNG imports made up about a quarter of total UK gas consumption in 2011, making the UK the world’s third biggest importer that year. On high demand days in winter, Ofgem said in its report that LNG supply overtook pipeline imports. This doesn’t look like it’s going to end any time soon – Ofgem expects gas supplies from European countries like Norway to decline in coming years.

But this situation could have important consequences. Ofgem warns that the UK’s level of dependence on LNG makes it vulnerable to shifts in supply and demand, as well as shocks in supply countries. For example, of the UK’s LNG imports in 2011, 87 per cent came from Qatar, which is a lot of gas from one place.

The UK’s lack of gas storage means it is even more exposed to potential shocks and price spikes, the Ofgem 2011 report says. The UK has less gas storage relative to our consumption than any other major

European economy and less of its gas is purchased under long term contracts, it adds.

Tighter markets and the gas price

According to Ofgem, increased global competition looks set to clash uncomfortably with increasingly sparse domestic supplies in the UK. Buchanan writes in the Telegraph today:

“[J]ust when we need more gas, world demand for gas is set to rise while our own supplies are predicted to fall by another 25pc by 2020.”

He explains that several factors are expected to tighten the availability of gas worldwide. For example, Russia’s large Shtokman field was cancelled last year. The project – located in the Russian Arctic – was set to be the country’s flagship shale gas production scheme. But costs spiralled out of control, European gas demand dipped due to the financial crisis, and US domestic gas prices dipped due to the shale gas boom.

But the most important trend in energy consumption will happen elsewhere. Asia is set to become the fastest-growing gas consumer. Buchanan says China’s consumption alone will grow at 20 per cent per year.

So what does all this mean for UK gas prices? Buchanan notes that while these combined demand spikes don’t look set to be sustained, they look set to strike in the run-up to 2020 – just “when we need gas for our power stations at record levels.”

Buchanan points out that the UK’s need for more LNG will mean it is exposed to Asian LNG prices, which “drive long-term contract prices” and are around 60 per cent higher than UK gas prices.” So without measures to reduce dependence on gas, higher prices are inevitable.

Shale gas

While gas prices elsewhere appear to be rising, the US is experiencing low prices due to the rise in domestic shale gas exploitation.

Some commentators have been arguing that the shale effect could do the same for global gas prices. But Buchanan says:

“It is true that the US has transformed its energy market thanks to shale, but in our time-frame, when Britain will rely on gas for its power stations, this is not going to happen on any significant scale either here or elsewhere in Europe.”

Buchanan says even if the US allows exports, it will still cost about as much as we pay now for winter gas – around £390 of the average gas bill, according to Ofgem’s latest figures.

So while there is plenty of gas out there, the question is how much of that will be available over the next five years – and how much the UK will have to pay to ensure it doesn’t go to one of the country’s increasingly attractive competitors.