What you need to know about PwCs shale oil findings

When it comes to promised energy revolutions – lower energy prices and changing geopolitics – shale oil has remained in the shadow of shale gas. But a new report by Pricewaterhouse Coopers suggests shale gas’s less popular oily little sister could come into its own in coming years, pushing down fuel prices and potentially boosting the world’s economy by up to $2.7 trillion. Here’s our read of the report – with graphs.

A US story – so far

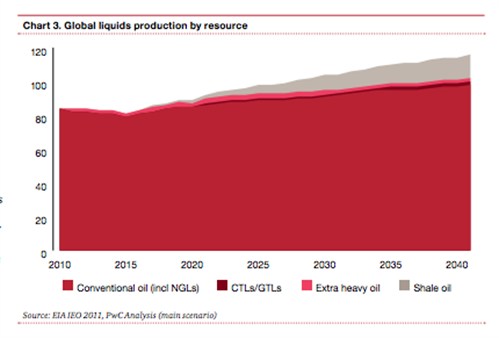

Just like shale gas, exploitation of shale oil – or light tight oil – has been concentrated in north America. And production has been accelerating – growing from 111,000 barrels per day in 2004 to 553,000 barrels per day in 2011. PwC says “shale oil could displace around 35-40 per cent of waterborne crude oil imports to the US”.

But PwC adds there’s also potential for production of relatively cheap oil to spread to other countries. It says early indications suggest there’s a lot of technically recoverable shale oil all over the world. PwC claims analyses from the International Energy Agency and the US Energy Information Administration (EIA) have been “arguably conservative” in their estimates of modest growth in global shale gas production.

By contrast, PWC ups the ante by extrapolating from available data and “drawing parallels with US shale gas experience” to conclude that shale oil could make up to 12 per cent of total oil supply by 2035.

Image - Screen Shot 2013-02-14 At 15.52.19 (note)

{kind=link}

Oil prices

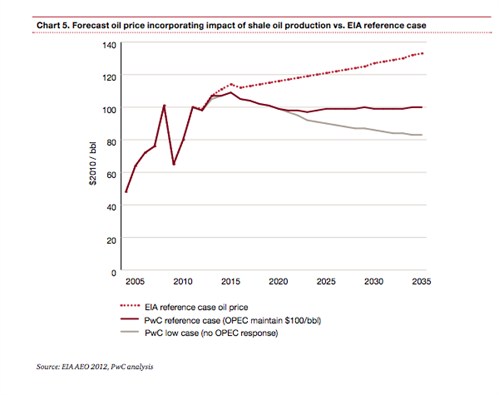

Shale oil could reach up to 12 per cent of global oil production and push prices down by between 25 and 40 per cent, PwC says.

The report is divided into two scenarios.

The “PwC reference case” allows for the association of the world’s biggest oil producers, OPEC, to respond to increases in shale oil production by limiting supply – meaning any oil price reduction would be limited.

The second scenario – the “PwC low case” does not include an OPEC response, so prices would fall lower, PwC says.

In both cases, PwC expects that the increase in shale oil production will force prices lower than the EIA expects. While the EIA has predicted oil prices will rise to around $133 per barrel by 2035, the PwC reference case predicts it will remain fairly steady at around £100 per barrel, while the low case sees prices falling to around $83 per barrel.

Image - Screen Shot 2013-02-14 At 15.12.36 (note)

{kind=link}

Cash injection

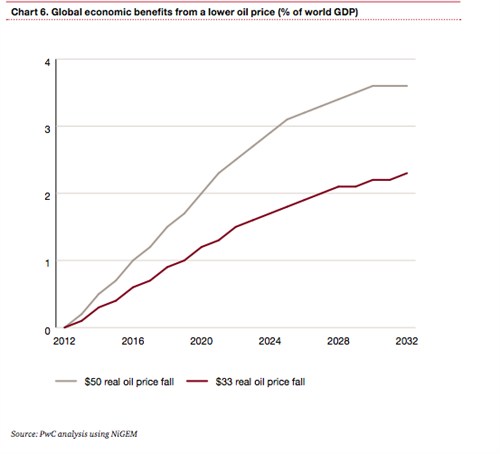

According to the report, the influx of of cheaper oil could add between 2.3 and 3.7 per cent to the global economy by 2035. It says: “At today’s GDP values, this is equivalent to an increase in the size of the global economy of around $1.7-2.7 trillion per annum.”

Industries that rely on oil – either to make things or to move things – could also benefit in the long term, PWC says. They include hauliers, heavy industry in general, the chemical industry, car makers and airlines.

Image - Screen Shot 2013-02-14 At 15.57.18 (note)Winners and losers

{kind=link}

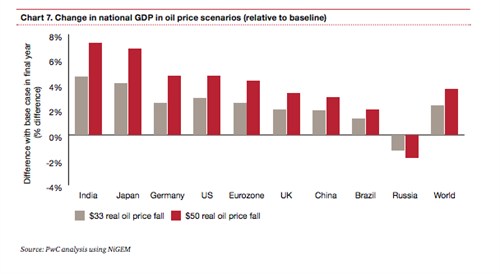

The big winners in PwC’s scenarios are expected to be the big oil importers. PWC predicts the largest net oil importers like India and Japan might see their GDP boosted by between four and seven per cent by 2035.

It could also boost consumers’ “real disposable income”, PwC says. It projects a $50 fall in the real oil price could increase private consumption per head by 2035 by more than $3,000 a year.

Image - Screen Shot 2013-02-14 At 15.01.31 (note)

{kind=link}

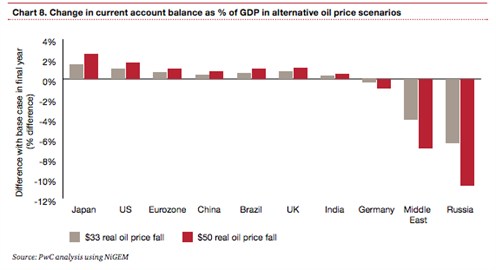

In contrast, major oil exporters like Russia and the Middle East could see their trade balances worsen by between four and ten per cent of GDP in the long run “if they fail to develop their own shale gas resources”, PWC warns.

Image - Screen Shot 2013-02-14 At 15.10.39 (note)

{kind=link}

Focus on the UK

PwC has also produced a handy video explaining what shale oil could do for UK energy markets. The report claims if global production of shale oil ramped up, the UK’s GDP could increase by up to $1240 (£800) per person by 2035.

It says estimates indicating there might be large reserves of shale gas under the UK suggest there’s potential for a lot of shale oil, too. This could ” contribute directly to investment, employment, economic growth and greater energy independence”, says PWC energy consultant Adam Lyons in the video.

He concludes:

“With North Sea resources in long term decline, we can create a new growth engine for UK plc if we seize the opportunity presented by the growth of this new resource in the UK and overseas.”

Haven’t we heard this before?

PwC admits that shale oil exploitation outside the US has so far been “disappointing” outside the US. In its report it assumes global shale gas exploitation will start scaling up from 2015, building to one million barrels per day by 2018 and “continuing to grow thereafter”, underpinned by a “supportive regulatory framework”.

James Leaton, research director at Carbon Tracker, tells Carbon Brief:

“Crucially, PWC’s report expects that it will be as easy to extract shale oil around the world as it has been in the US. Yet we know from experience that this might not be the case. Predictions that shale gas would be exploited worldwide in the same way as it is in America haven’t panned out – and US shale gas has yet to bring the global cost of gas down”.

The catch

Unlike shale gas, which has helped reduce the US’s carbon footprint by displacing much more polluting coal, shale oil isn’t going to have any relative emissions benefits. PWC warns affordable oil could conflict with decarbonisation and it’s careful to point out that without strong policies in place, this could be bad news for the world’s carbon emissions.

But policies aimed at cutting carbon could put a dampener on shale oil production. Carbon Tracker released a report last year highlighting that markets so far haven’t cottoned on to the fact that high carbon businesses’ models could come unstuck if governments get serious about constraining carbon emissions. Leaton says:

“Shale oil has the potential to extend oil production, but that will still depend on carbon constraints. If governments introduce carbon cutting policies, that will lead to reduce demand and oil prices. Adding that up knocks out around 40-60 per cent of the value of the European oil majors, according to recent analysis by HSBC.”

It’s important to remember that extracting shale oil is still an energy and resource-intensive process. Leaton adds:

“It’s worth asking whether this is a sensible use of resources and capital or whether we want to put those resources into investments that give a better return.”