International Energy Agency: No gas revolution before 2020

Gas markets could face tough times for the rest of the decade, a new report says.

The International Energy Agency (IEA) projects gas growth to be slower than previously expected. Countries across the Atlantic are failing to replicate North America’s shale gas ‘revolution’, while the import market is becoming increasingly tight in response to growing global demand.

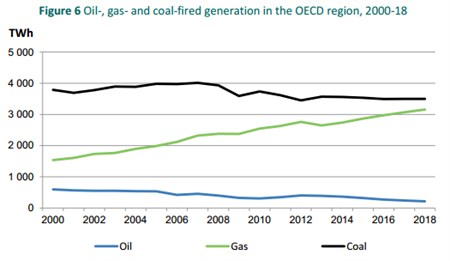

Gas and coal converge

Gas is expected to edge out coal and oil power generation over the rest of the decade, as the graph below shows:

Image - IEA gas report, gas vs coal (note)

{kind=link}

{kind=link}

But the IEA doesn’t expect gas to grow at at quite the pace it previously suggested – revising down its growth estimate from 2.7 per cent per year until 2018, to 2.4 per cent.

While that’s not a large drop, it does suggest the gas market isn’t quite as healthy as the IEA previously thought.

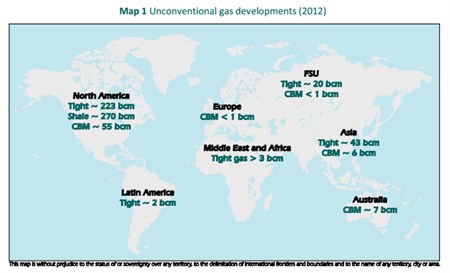

No global unconventional gas revolution

The new report also suggests the US’s shale gas boom isn’t likely to be replicated elsewhere any time soon.

That news will disappoint some in the UK – including the Treasury – that were hoping a domestic ‘ dash for gas‘ could mean reduced import dependence.

The IEA calculates 90 per cent of the world’s shale gas, tight gas and coal bed methane production was in the US in 2012, as the map below shows:

Image - IEA unconventionals (note)

{kind=link}

{kind=link}

Other regions are lagging behind because they are yet to be convinced fracking is safe, the IEA says. Europe is a particularly sad shale story: the IEA is disappointed by inertia in Poland and continuing political opposition in France and Germany.

It’s more positive about shale gas prospects in the UK, however. It says the government’s decision to end a moratorium on shale gas exploration “stands out as a beacon” in Europe’s progress during 2012.

While that kind of praise will please the Chancellor, George Osborne, there are still plenty of obstacles to the development of a UK shale gas industry. The IEA acknowledges unconventional gas production “is and will remain a mainly North American… story” in the coming years. It explains:

“the unique circumstances (favourable geology, liquid gas market, private land ownership, lower population density, well-developed infrastructure) that allowed the US shale gas boom to happen so quickly do not always exist in other markets”.

So the UK is will probably import the vast majority of its gas for some time yet.

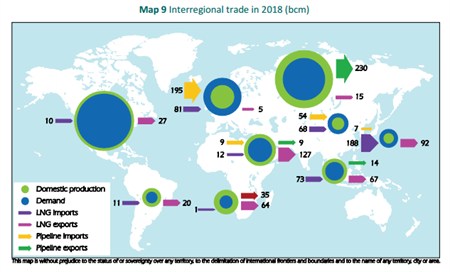

Growing demand tightens export market

Supplies of one type of gas export – liquefied natural gas (LNG) – are expected to run low in the next few years, the IEA warns.

Few LNG projects are set to be completed in the next two years while global demand is set to increase, leading to shortages.

The map below shows how the IEA expects gas to flow in 2018:

Image - IEA gas, trade map (note)

{kind=link}

{kind=link}

Growing demand in the Middle East and Africa is expected to swallow most of the region’s LNG supply, leaving Europe to rely on pipeline imports from Russia until around 2017 – a scary prospect for some governments. But by 2018 more LNG is expected to be available, allowing Europe to wean itself off Russian gas.

The end of the “Golden Age” of gas?

Despite these challenges, the IEA’s executive director Maria van der Hoeven remains optimistic “the ‘Golden Age’ of gas remains in full swing”. Nonetheless, slower growth and supply difficulties mean global gas production is starting to look more like a waltz than a full-blown jive.